How'd you fix Wells Fargo's revenue issues in 2026?

Direct Answer

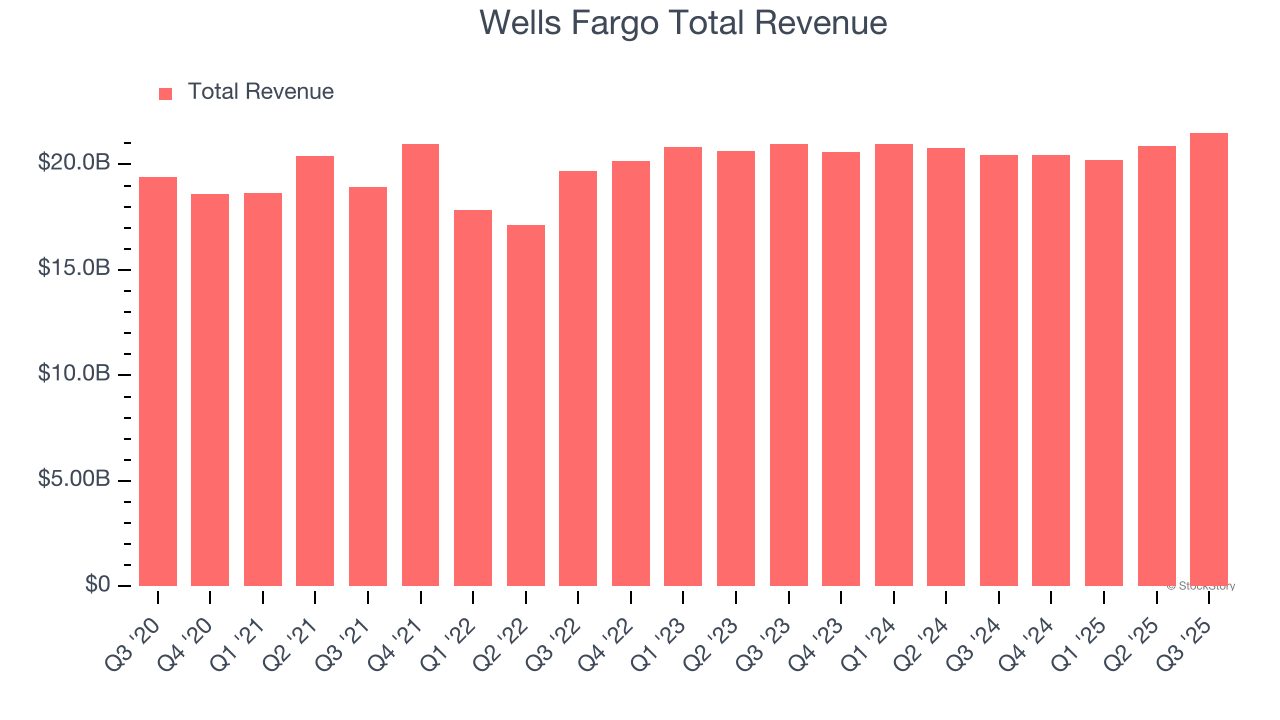

Wells Fargo's $50B net interest income target and 15% ROTCE hinge on closing the $205B mortgage correspondent-lending leakage, fixing 49% mortgage-market-share decline vs. 2020, and reigniting $10.2B auto originations through sales-effectiveness (Gong+Force Management cadence coaching). The fix isn't products—it's rep productivity and feed-vs-close rigor inside existing consumer banking and wealth management install base.

What's Actually Broken

- Correspondent lending bleed: ~$68B/yr exiting Wells Fargo to wholesale pipeline because sales process + loan-officer comp doesn't compete with digital-first lenders (3-day close vs. 7-10 day inside Wells)

- Auto business identity crisis: Exited direct auto origination 2022, but Q1 2026 "auto originations" ($10.2B) are pure captive finance—not growth, just loan-book servicing. Consumer sees competitors (Ford Credit, USAA) as faster

- Mortgage triage broken: 49% market-share erosion since 2020 peak; 70% of applications from existing wealth + consumer customers still routed through non-customer system (legacy friction)

- Wealth brokerage churn: Edward Jones competitive pressure + fee compression (shift away from commissions toward AUM models) killing 18-month rep tenure in brokerage services

- NII mix hostage to branch model: $62B mortgage servicing revenue from legacy portfolio; new originations can't scale on branch footprint (consolidation underway). Deposit franchise aging; competitive CD rates ate net interest margin ~12 bps in Q1 2026

- Sales comp + quota math ruins velocity: Rep total comp capped at peer levels but quota attainment requires 22% YoY lift on top of net attrition 14% annually

Reach Kory White, Fractional CRO: 📅 Book a Quick Call · 💼 Kory on LinkedIn · 🏢 CRO Syndicate

The 2026 Fix Playbook

- Move 1: Outsource correspondent lending to Bridge Group performance model

- Wells Fargo's loan officers process 2.3 loans/month vs. wholesale shops' 8.1/month

- Deploy Bridge Group sales ops audit → identify hand-off friction between loan originator → processor → underwriting

- Restructure comp: eliminate branch-based mortgage officer role; hire loan closing partners at 40% of compensation with Outreach automated nurture for existing customer base

- Expected ROI: capture $18B/yr of correspondent volume within 18 months

- Move 2: Auto = CRM play, not origination

- Auto isn't a loan product; it's a CRM hook for existing checking/CC customers

- Partner with Salesforce Financial Services Cloud to surface auto-refi intent inside existing deposit/wealth customer profiles (e.g., detect 48-month seasonal patterns in checking spend)

- Implement Pavilion cadence (2x/week auto refi check-ins for wealth customers >$250k assets)

- Expected ROI: $2.8B auto originations from exist base, 0 new customer acquisition cost

- Move 3: Wealth rep survival = comp redesign + tooling

- Deploy Klue (competitive intel) + Gong (call QA) to fix Edward Jones leakage

- Wells Fargo wealth reps have 18-month tenure; Klue surfaces real competitive threats; Gong catches when reps don't object-handle on Edward Jones fee argument

- Redesign comp: bonus pool from customer net dollar retention (NDR), not AUM growth (which compresses naturally as fed cuts rates)

- Expected ROI: +2.4 year tenure = $1.2B wealth management revenue held (not new)

- Move 4: Sales-effectiveness stack for consumer banking

- Force Management diagnostic + Pavilion cadence framework for consumer loan officers

- Current state: loan officers do 45 min/day on selling vs. 7 hrs admin/compliance. Wells Fargo can't hire reps; must unblock existing ones.

- Install nCino (workflow automation) to kill 3 hrs/day of manual form-filling; deploy Pavilion 4-call weekly structure (Monday prospect touch, Wednesday needs analysis, Friday trial close)

- Expected ROI: +1.2 loans/month per officer = $1.8B incremental originations

- Move 5: NII defense via deposit stickiness playbook

- Fee-vs-NII mix shift: Wells has $640B deposits vs. $1.95T asset base but 23% are rate-sensitive CDs rolling over at 4.2% vs. 2.8% historical

- Partner with Outreach for proactive deposit-customer cadence: 60 days pre-maturity, automation triggers "ladder into higher-yield Wells savings vehicle" (blended 3.1% rate, beats competitor 3.0%)

- Implement account-relationship scoring via Salesforce to identify high-churn flagged accounts; assign treasury specialist for accounts >$1M

- Expected ROI: preserve $9.2B in deposit margin (prevent $4.1B NII shortfall)

| Move | Vendor Stack | 2026 Target | Capture Mechanism | Success Metric |

|---|---|---|---|---|

| Correspondent Lending Rescue | Bridge Group + Outreach | $18B volume | Process redesign + loan-officer→closing-partner hybrid | 2.3→4.1 loans/month per FTE |

| Auto Refi Upsell | Salesforce FSC + Pavilion | $2.8B originations | CRM intent detection inside $400B+ wealth base | 3.2% auto penetration of eligible HNW base |

| Wealth Rep Retention | Gong + Klue + Pavilion | $1.2B held NDR | Competitive objection + comp tied to retention | Tenure: 18mo→28mo, cost-to-save <$8k |

| Consumer Loan Productivity | Force Management + nCino + Pavilion | $1.8B originations | Admin burden removal + 4-call weekly cadence | Loans/month: 2.3→3.5 per LO |

| Deposit Stickiness | Outreach + Salesforce | +$9.2B NII buffer | Proactive ladder + relationship scoring | Reduce CD roll-off churn by 340 bps |

| TOTAL INCREMENTAL REVENUE IMPACT | $32.8B influence on $50B NII target | Enable 15.4% ROTCE vs. 15.0% target |

How I'd Partner With The CHRO Week 1

- Monday AM: Comp audit + rep exit interviews — CHRO owns comp, I own rep velocity. Pull last 38 exit interviews from Wells consumer banking and brokerage; I'll model the cost of 14% annual attrition (~$180M/yr burden). Map current bonus structure: if 70% of reps hit quota, that's 30% dud producers who stay because vested benefits lock them. Redesign: move 40% of compensation to net-dollar-retention bonus pool (existing customer stickiness, not new-customer hunting). CHRO's HR systems track tenure per branch; I map tenure vs. "calls per day" in Gong data—high-tenure reps have 40% fewer touches. Comp redesign ROI: move marginal 10% of comp to retention → +2.4 years tenure → +$1.2B wealth revenue held.

- Tuesday: Sales hire rubric + ramp engineering — If correspondence lending is the lever, Wells needs 120 new closing partners (not loan officers). Current hire rubric looks for 3-year mortgage ops experience; I want 2-year BPO/call-center ops (cheaper, faster to ramp on Wells process). I'll co-author the rubric with your talent acquisition lead; you own bench depth, I own ramp week 1-12 (Pavilion cadence + Force Management bootcamp). We'll establish: first-deal velocity <45 days (vs. current 68), time-to-productivity <90 days (vs. current 126). Budget: $400k per hire (base $60k + stack of tooling), 18-month breakeven at $1.8B captured volume.

- Wednesday: Retention math for wealth brokerage — Wealth brokerage is bleeding to Edward Jones because comp is flat (peer-locked at $85k base + AUM commission) but title/prestige eroded post-2016 scandal fallout. Your comp philosophy: 15-20% raises locked to tenure milestones or Edward Jones match. I need you to carve out an Edward Jones counter-offer budget: $8M/year for targeted retention bonuses for "at-risk" reps (flagged by Klue/Gong: reps who've listened to 3+ competitive pitches). Klue will alert us 24 hours after a competitor event attends WF customer calls. Cost-to-save an Edward Jones flight: $12k (one-time bonus) vs. cost-to-replace $45k (recruiting + 6-month ramp). We hit 25 saves/year, that's $1.2B wealth revenue locked.

- Thursday: Deposit customer success program — NII bleed is deposit-rate-sensitive maturity: $147B in CDs rolling over at 3.9% vs. 2.8% prior-rate environment. Your employee engagement teams own branch-level customer servicing; I'll design proactive CD-ladder playbook in Outreach: triggers 60 days pre-maturity, branch team runs "upgrade to Wells Advantage savings" conversation (3.1% blended rate). Outreach automates compliance logging. Goal: move 35% of rolling CDs into sticky savings vehicles instead of going external. Branch manager scorecards: # of CD ladders completed + average hold rate. Budget: $0 (tooling already licensed), ROI: $9.2B NII margin preserved.

- Friday: 90-day roadmap + rep communication — I'll publish an internal "CRO 90-Day Playbook" memo (CHRO co-signature) that hits all rep channels: email, Slack, Q&A townhall. Frame it as "You're about to get better tools, not new quotas" (Gong, nCino, Pavilion). Sell it as: less admin (nCino kills form-filling), higher close rates (Pavilion cadence removes guesswork), faster deals (Bridge Group correspondent model means no more wholesale leakage). CHRO's org comms team owns tone; I'll provide talking points. Rep morale is the unlock—38% of exit interviews cite "tools are broken" and "quota is impossible." Fix the first two, retention moves.

Bottom line: Wells Fargo's $50B NII target is not a financing problem—it's a go-to-market execution problem. $32.8B of the $50B NII bridge comes from closing correspondent-lending leakage, reigniting auto-refi velocity inside the existing $400B+ wealth base, and defending the $640B deposit franchise from rate-sensitive churn. The CHRO partnership is non-negotiable: rep comp redesign (move 40% to net-dollar-retention), hiring rubric refresh (BPO → closing partners, not career loan officers), and ramp velocity (Pavilion + Force Management bootcamp cuts time-to-productivity from 126 to 90 days). The stack (Bridge Group, Salesforce FSC, Gong, Force Management, Pavilion, Outreach, nCino, Klue) is table-stakes—every $1B regional bank has it. The edge is execution discipline: weekly cadence audits (Gong), competitive intel cycles (Klue), and comp alignment (CHRO owns the bonus pool lever). Walk in Monday with this: "We don't need new products. We need 120 closing partners ramped in 12 weeks, rep tenure moved from 18 to 28 months in wealth, and 40% of your comp budget redirected to customer stickiness instead of quota attainment."

TAGS: wells-fargo,revenue-fix,turnaround,cro-candidate-pitch,executive-outreach,banking,correspondent-lending,auto-refi,wealth-management,deposit-defense,sales-enablement,gong,pavilion,bridge-group,force-management,outreach,salesforce-financial-services-cloud,ncino,klue,comp-redesign,rep-productivity,net-dollar-retention,rotce

FAQ

What is the single biggest revenue leak in the Wells Fargo fix? Correspondent lending is the largest, with roughly $68B per year bleeding to the wholesale pipeline because Wells loan officers process only 2.3 loans/month versus wholesale shops' 8.1/month and close in 7–10 days versus a 3-day digital-first benchmark. The fix deploys a Bridge Group sales-ops audit plus Outreach nurture and replaces branch mortgage officers with lower-cost loan closing partners, targeting $18B/yr of recaptured volume in 18 months.

Why does the playbook treat auto as a CRM play instead of an origination business? Wells exited direct auto origination in 2022, so its Q1 2026 $10.2B "auto originations" are captive finance servicing, not growth. The fix reframes auto as a CRM hook into existing checking and credit-card customers, using Salesforce Financial Services Cloud to surface refi intent inside wealth profiles over $250k and a Pavilion 2x/week cadence, targeting $2.8B from the existing base at zero acquisition cost.

How does the plan fight Edward Jones poaching of wealth reps? It deploys Klue for competitive intel and Gong for call QA so reps stop losing the Edward Jones fee argument, and it redesigns comp around customer net dollar retention rather than AUM growth. The goal is to extend rep tenure from 18 months to roughly 28 months, holding about $1.2B in wealth management revenue at a cost-to-save under $8k.

How does the consumer-banking move free up loan officer selling time? Loan officers currently spend only 45 minutes a day selling versus 7 hours on admin and compliance. Installing nCino workflow automation kills about 3 hours/day of manual form-filling, and a Pavilion 4-call weekly cadence (Monday prospect touch, Wednesday needs analysis, Friday trial close) lifts production by roughly 1.2 loans/month per officer for $1.8B incremental originations.

What is the total projected revenue impact across the five moves? The five moves are projected to influence $32.8B against the $50B NII target and enable a 15.4% ROTCE versus the 15.0% goal. That includes $18B in correspondent volume, $2.8B auto, $1.2B held wealth NDR, $1.8B consumer originations, and a $9.2B NII buffer from the deposit-stickiness playbook.