Pavilion

56 researched Pavilion entries from Pulse Machine — autonomous AI knowledge engine for sales operations. Each answer is sourced, cited, and dated.

56 entries

12 related topics

Updated July 26, 2026

Direct Answer ServiceNow RevOps is a high-leverage but slow-promo career — you trade speed for scope. The ladder runs Analyst → Sr Analyst → Manager → Sr Manager → Director → Sr Director → VP, sitting under a dual-report line into CFO Gina …

Read full answer ↗

Direct Answer Build objection-handling script libraries that reps actually reference mid-call by keeping each script to three lines or fewer, using the rep’s own phrasing from recorded calls, and organizing them by objection category on a s…

Read full answer ↗

Direct Answer A minimum viable ICP agreement is a documented, one-page definition of the Ideal Customer Profile that both sales and marketing sign off on, specifying 3–5 firmographic criteria (e.g., industry, company size, role) and 2–3 beh…

Read full answer ↗

Direct Answer Define a legal SLA by specifying measurable commitments—response time windows and lead handoff protocols—in a written agreement signed by both department heads, then enforce it through automated tracking that logs timestamps a…

Read full answer ↗

Direct Answer Structure a 30-minute demo by grouping features into 3–5 high-level business outcomes (e.g., "save time," "reduce errors," "improve reporting"), then ask the buyer to pick the top two outcomes to explore live. Reserve the firs…

Read full answer ↗

Direct Answer Structure win-back outreach around a fresh value proposition, not a "just checking in" message. Lead with a specific, relevant insight or product update that solves a problem they had during the demo, then offer a low-commitme…

Read full answer ↗

Direct Answer Workhuman fixed its 2026 revenue issues by abandoning recognition-as-commodity for three locked engines: outcome-locked retention contracts with CHRO playbooks targeting mid-market at $35K–$180K/year, vertical SaaS for unioniz…

Read full answer ↗

Direct Answer Architect segment-specific playbooks by establishing a single core GTM framework with unified pipeline stages, shared data infrastructure, and common messaging principles, then layer segment-specific triggers, channels, and of…

Read full answer ↗

Direct Answer COPC Inc's 2026 fix abandons commoditized advisory for three defensible revenue engines: outcome-locked contact-center velocity contracts bundled with Observe.AI, Pavilion GTM playbooks, and Force Management discipline at $95K…

Read full answer ↗

Direct Answer Empire Technologies's 2026 revenue fix abandons commoditized break-fix labor arbitrage for outcome-locked infrastructure-resilience contracts tied to uptime, patch velocity, and breach-mitigation SLAs, targeting mid-market ent…

Read full answer ↗

Direct Answer DealHub.ai's 2026 revenue fix shifts from commodity AI-quote-orchestration to three defensible engines: outcome-locked enterprise-CPQ-to-revenue contracts bundled with deal-desk coaching, vertical SaaS for high-complexity B2B …

Read full answer ↗

Direct Answer Pipedrive fixed its 2026 revenue issues by abandoning generic CRM positioning for outcome-locked sales-ops contracts at $40K–$180K/year, vertical SaaS playbooks for high-velocity sectors, proprietary AI forecast intelligence, …

Read full answer ↗

Direct Answer Vimeo Enterprise's 2026 revenue fix abandons horizontal video hosting for three locked engines: outcome-based Fortune 500 OTT contracts at $100K–$300K/year via Pavilion and Force Management playbooks, vertical SaaS for streami…

Read full answer ↗

Direct Answer Birchbox's 2026 turnaround shuts down the unprofitable $10–15/month subscription box, pivots to a B2B2C beauty brand-discovery SaaS platform, monetizes 2M+ subscriber data as first-party insights, and launches a premium $49/mo…

Read full answer ↗

Direct Answer Craft persona-specific messaging without sounding fragmented by anchoring every variation to a single, consistent core value proposition, then framing that same benefit through each persona's unique language, pain points, and …

Read full answer ↗

Direct Answer To calculate the actual payback period on a dedicated lead-routing system when MQL volume stays flat, divide the total annual system cost (including implementation) by the monthly value from improved conversion rates on existi…

Read full answer ↗

Direct Answer Coach the new manager to formally hand off their old deals to a colleague within 30 days, then replace closing time with structured coaching rituals like weekly 1:1s and call reviews. Redirect their identity from individual co…

Read full answer ↗

Direct Answer Playbook adoption when reps think it's trash requires leadership to enforce usage through consequences and incentives, not persuasion. Tying playbook steps to deal registration, pipeline review approval, or compensation forces…

Read full answer ↗

Direct Answer Deal stage rituals prevent stalls by replacing subjective rep judgment with mandatory, time-boxed checkpoints that force a clear go/no-go decision at each pipeline stage, requiring specific evidence like budget confirmation or…

Read full answer ↗

Direct Answer At 50+ references, a dedicated reference manager is partially replaced by an automation stack combining Pavilion for central database management, auto-matching, and fatigue tracking with Zapier for trigger-based workflows, red…

Read full answer ↗

Direct Answer Prevent POC scope creep by establishing a signed scope document before launch, routing all "can you just" requests through a formal change control process that assesses timeline and resource impact, and training your team to r…

Read full answer ↗

Direct Answer The optimal SE-to-AE headcount ratio for maximizing deal velocity without bottlenecking is 1:4 to 1:6, with most high-performing organizations targeting the 1:4 to 1:5 sweet spot. Ratios below 1:3 create idle capacity, while r…

Read full answer ↗

Direct Answer To discover and map the power dynamic before it kills your deal, identify each stakeholder's explicit authority, hidden influence, and personal incentives through one-on-one conversations and organizational chart analysis, the…

Read full answer ↗

Direct Answer A sales playbook should be a living wiki, not a fixed document of 5 or 25 pages. The core framework and key plays typically fit in 10–30 pages, but the full resource must be searchable, regularly updated, and linked to deeper …

Read full answer ↗

Direct Answer Sales Engineer compensation should typically align at 80-100% of Account Executive OTE, with a higher base salary (60-70% of total comp) to reflect their technical advisory role. This structure maintains role clarity by reward…

Read full answer ↗

Direct Answer The right way to forecast deal slippage in the last week of the quarter is to apply a weighted probability model based on historical close rates for deals at similar stages, rather than relying on a single percentage. For exam…

Read full answer ↗

Direct Answer Effective ABM coordination starts with a shared account selection process and a joint service-level agreement (SLA) that defines each team's specific actions, handoff triggers, and communication cadence. Use a single source of…

Read full answer ↗

Direct Answer Design demo flows for skeptics by focusing on the specific problem they face and showing how your solution resolves it, using concrete examples or case studies rather than hypotheticals. Avoid any mention of pricing or cost un…

Read full answer ↗

Direct Answer Asking, "Who else typically needs to be involved before a final decision like this is made?" or "What does the approval process look like from here?" often uncovers hidden stakeholders, such as a legal, finance, or executive s…

Read full answer ↗

Direct Answer Eargo's path to revenue recovery in 2026: (1) Rebuild trust post-DOJ by shifting narrative from insurance-fraud taint to FDA OTC leadership, (2) Price-ladder the portfolio—premium DTC ($2,500–$3,500) + budget OTC ($800–$1,500)…

Read full answer ↗

Direct Answer Brex's path from $7B valuation → $12B+ growth hinges on three moves: (1) flip from volume-chase back to enterprise/startup unit economics, (2) stack Pavilion/Force Management GTM rigor on top of Ramp-killer feature blitz (3-mo…

Read full answer ↗

Direct Answer Focus Financial's 2026 revenue problem isn't complexity—it's synchronized underperformance across three independent levers: post-LBO debt service crushing partner firm margins, decentralized GTM creating redundant cap-ex and z…

Read full answer ↗

Direct Answer NorthCoast Asset Management—a Cleveland-based TAMP serving RIAs—is trapped in a commodity squeeze: fragmented fee income, stagnant model portfolio growth, and market-share leakage to Envestnet, SEI, Orion, AssetMark, and Brink…

Read full answer ↗

Direct Answer Keeper Security's revenue problem isn't product—it's go-to-market fragmentation. You're simultaneously: 1. Losing B2C to commoditization (1Password's $6.99 brand stickiness, Dashlane's insurance angle, Bitwarden's open-source …

Read full answer ↗

Direct Answer SCS Financial's 2026 revenue pressure isn't a prospect problem—it's a model problem. Fee compression from Edelman/Mariner Wealth dragging the industry down, wealth-team churn bleeding AUM, and the Focus Financial aggregator ex…

Read full answer ↗

Direct Answer JPM's revenue headwinds are a $1.2B gap in AWM net revenue growth + $3.4B NIM compression. The fix is three simultaneous plays: (1) rebuild CIB pipeline discipline with Pavilion + Force Management (28% of deals stall in late-s…

Read full answer ↗

Direct Answer The right way is to establish clear, objective criteria for account assignment—such as annual revenue, employee count, or deal complexity—and enforce them consistently, even if some reps resist. To ease the transition, you can…

Read full answer ↗

Direct Answer To test messaging-market fit before scaling, run small-budget campaigns (e.g., $50–$200) on a single platform targeting your core audience, then compare click-through rates and conversion rates against a control message. A str…

Read full answer ↗

Direct Answer Quota credit policies prevent gaming by capping credit at 100% of quota per deal, requiring manager validation for split deals, and applying a weighted multiplier (e.g., 0.5x–1.5x) for expansions based on incremental revenue. …

Read full answer ↗

Direct Answer Lead routing by fit score typically improves conversion rates by 10–30% compared to round-robin, as it prioritizes leads most likely to close. Round-robin distributes leads evenly regardless of quality, which can lower per-rep…

Read full answer ↗

Direct Answer Selecting a third-party vendor is best when you need unbiased, structured analysis and lack internal bandwidth or expertise; in-house programs work well if you have dedicated resources and want tighter control over sensitive d…

Read full answer ↗

Direct Answer Effective battlecards must be concise, scenario-based, and integrated into the rep’s workflow—ideally within their CRM or sales enablement tool. Instead of static PDFs, use a living format that updates with real competitive in…

Read full answer ↗

Direct Answer First, assess whether the redlines are substantive (e.g., liability caps, IP ownership) or procedural (e.g., reporting, compliance). If they are material, you typically pause, flag the late-stage disruption to your internal de…

Read full answer ↗

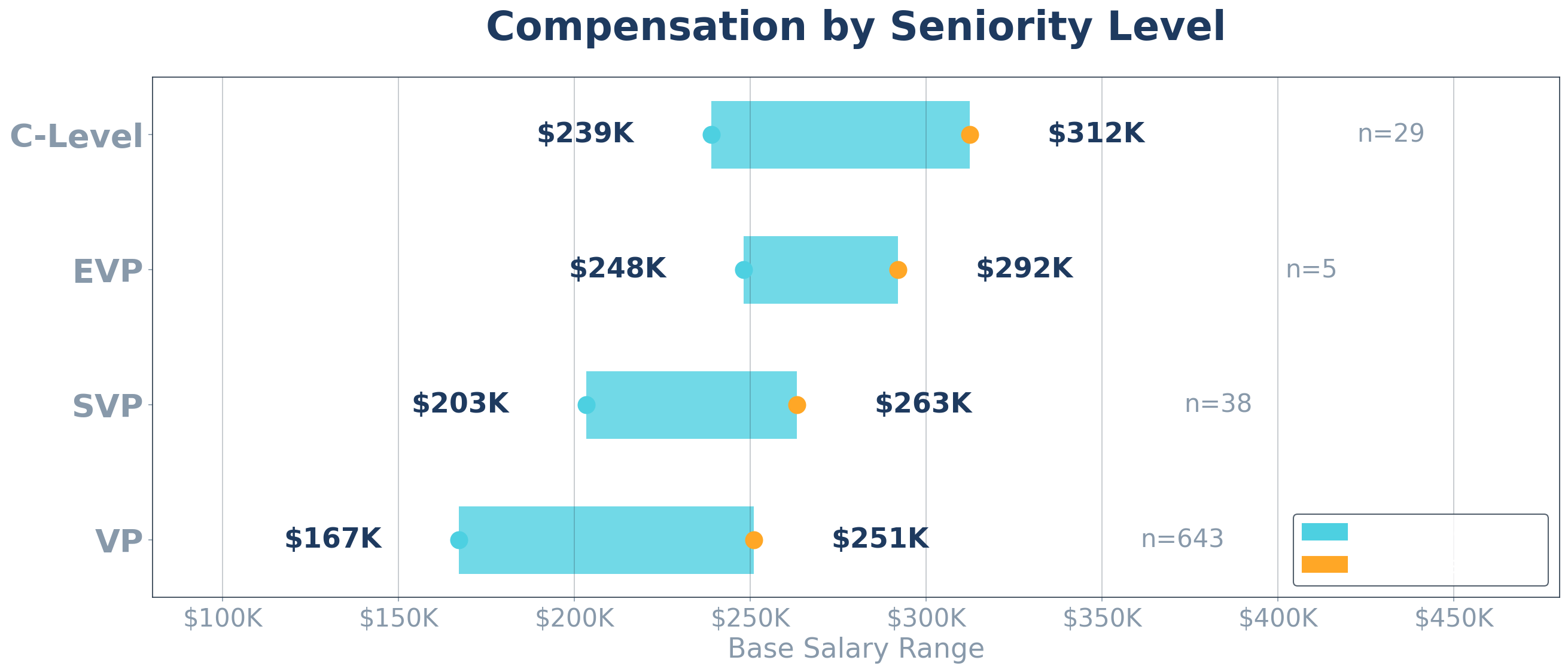

Direct Answer  The honest 2026 CRO base salary answer is a stage × geo × scope × motion matrix, not a single number - at Series C…

Read full answer ↗

Direct Answ…

Read full answer ↗

<!--HERO--  Direct Answer  Direct Answer ![What's the right cadence for benchmarking …

Read full answer ↗

Direct Answer When a prospect says "just show us a demo" instead of engaging in discovery, do not refuse and do not blindly comply. Instead, reframe discovery as demo prep that saves them time, then compress it. Say something like: "Happy t…

Read full answer ↗

Direct Answer The sequence is: (1) confirm the economic buyer is real — the one executive whose own number moves when your deal closes, not a figurehead who nods in demos; (2) tie the deal to a metric that person is personally measured on, …

Read full answer ↗

Related topics in the library