Pulse Reviews and Analysis

Pulse Reviews and Analysis

Top 10 Data Center REIT Revenue KPIs

Curated by Kory White · Fractional CRO, CRO Syndicate

Curated by Kory White · Fractional CRO, CRO Syndicate

Direct Answer

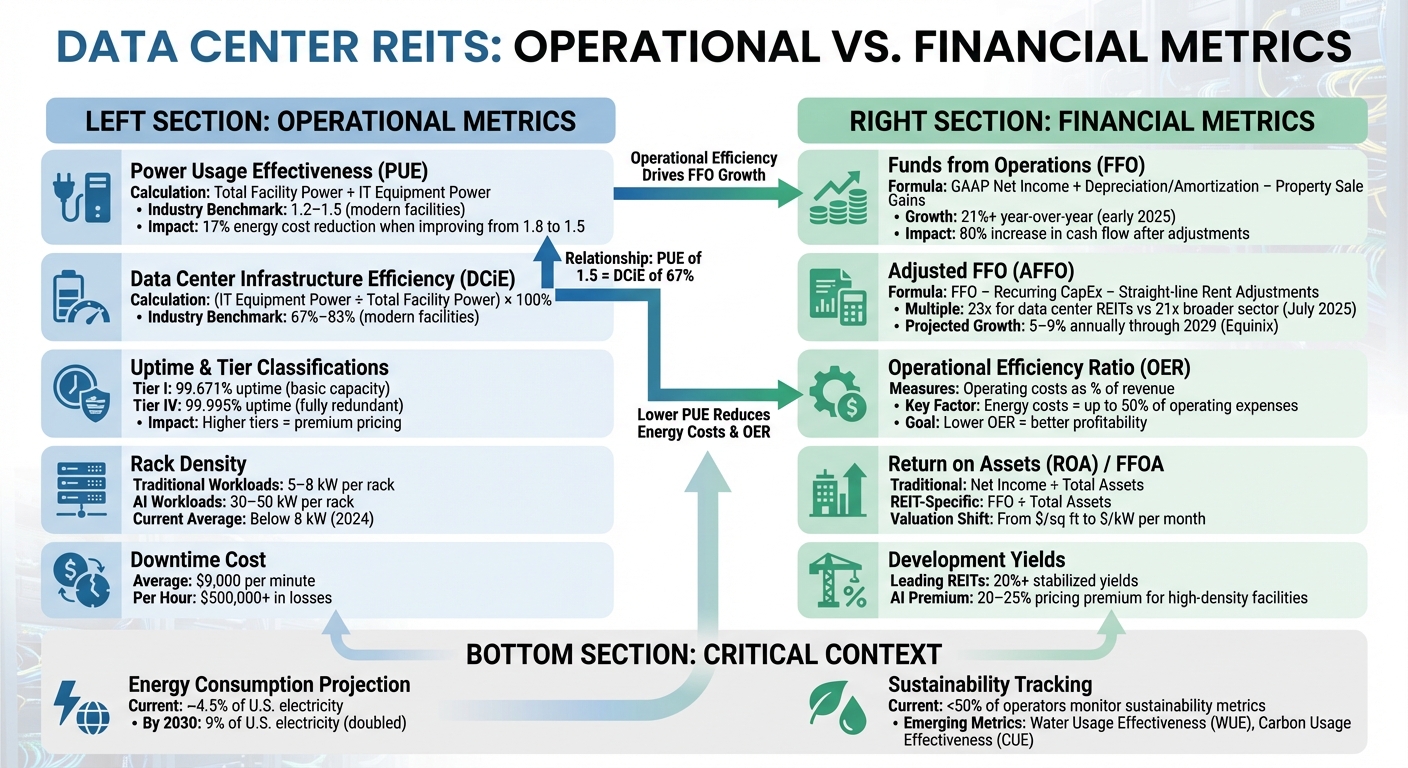

Data Center REITs (Real Estate Investment Trusts) operate a unique hybrid business: they sell real estate capacity (square feet, power) and a technology service (uptime, connectivity). Their revenue KPIs must therefore blend real estate occupancy metrics with technology service-level metrics.

The top KPIs focus on power utilization, lease structures, churn, and capital deployment efficiency.

Why Data Center REITs Work Differently

Data center REITs differ from traditional office or industrial REITs because their core asset is power availability, not just floor space. A tenant might lease 10,000 square feet but need 5 MW of critical power. If the REIT cannot deliver that power, the space is worthless.

Conversely, a data center can have high physical occupancy but lower power utilization, meaning significant revenue potential is left on the table.

This leads to a dual measurement system: real estate KPIs (occupancy, rent per square foot) and infrastructure KPIs (power usage effectiveness, megawatt capacity leased). The revenue model is also more complex because tenants often pay for power separately from space, creating a pass-through revenue stream that carries low margin but high volume.

Another key difference: data center leases are commonly structured so that the tenant bears power, maintenance, and operating costs, but with a twist — the REIT often procures power wholesale and passes it through to tenants. This creates a power cost of goods sold (COGS) that must be tracked separately from rent revenue.

Power and cooling costs are a large share of a data center's operating expense base, which is why power procurement and pass-through structures are a central financial concern for the sector.

Finally, data centers are capital-intensive with long construction lead times (often 18–36 months). Revenue KPIs must account for pre-leasing (leasing space before construction is complete) and the development pipeline (future revenue from projects under construction). This is unlike a traditional office REIT where you lease completed space.

The 10 KPIs, In Depth

1. Revenue per MW (Megawatt)

Definition: Total rental revenue divided by total contracted megawatts of critical power.

Why it matters: It normalizes revenue across different facility sizes and power densities. A 10 MW facility with $20M in annual rent has a Revenue per MW of $2M. This allows comparison between a legacy colocation facility (lower density) and a hyperscale facility (higher density, typically lower revenue per MW but larger scale).

How to calculate: (Total annualized rental revenue) / (Total contracted MW). Exclude power pass-through revenue to avoid double-counting. Wholesale and hyperscale capacity generally prices at a lower revenue-per-MW than retail colocation, which carries interconnection and service premiums.

2. Occupancy Rate (by Power)

Definition: The percentage of total available critical power capacity that is under contract. This is distinct from physical occupancy (square feet leased).

Why it matters: A data center could be near-full physically but lower on power if tenants are contracted for less power than the facility can deliver, or are ramping into contracted capacity. Tracking both occupancy measures exposes over-provisioning and unused-but-saleable capacity.

Why two numbers: Power occupancy and physical occupancy can diverge meaningfully. A gap between the two is often the clearest signal of latent revenue — capacity that is built and powered but not yet leased or ramped.

3. Average Lease Term (Weighted by Revenue)

Definition: The average remaining term of all leases, weighted by the revenue each lease generates. This measures revenue stability and predictability.

Why it matters: Data center leases commonly run 3–10 years, and hyperscale leases can run much longer (10–15 years). Longer terms reduce churn risk and provide visibility into future cash flows; shorter terms increase flexibility but also increase re-leasing risk.

How to calculate: Sum of (lease revenue * remaining term in years) / Total revenue.

4. Churn Rate (by Revenue)

Definition: The percentage of revenue lost due to tenants not renewing leases or terminating early, measured over a 12-month period.

Why it matters: Data center churn is expensive because it leaves power and space idle while fixed costs (cooling, security, maintenance) continue. High churn forces the REIT to spend on tenant improvements and leasing commissions to backfill.

Benchmark: Industry churn typically runs in the mid-single digits annually; well-run operators target the low single digits. A churn rate that climbs into double digits is a red flag for pricing pressure or service issues.

5. Net Effective Rent (NER)

Definition: Total rent revenue minus all tenant concessions (free rent, tenant improvement allowances, leasing commissions) divided by the lease term. This is the true revenue per unit of space or power.

Why it matters: Data center leases often include months of free rent for build-out. NER strips out these incentives to show real revenue. For a lease with a $250,000/year face rent, NER might land meaningfully lower after concessions are amortized across the term.

6. Power Utilization Rate (PUR)

Definition: The ratio of actual power consumed by tenants to the total contracted power capacity. This measures how much of the leased power is actually being used.

Why it matters: Tenants often lease more power than they initially need (e.g., reserving capacity for future growth). If utilization is low relative to contracted capacity, the REIT may have upsell or right-sizing opportunities. It is a leading indicator of where contracted-but-unramped capacity sits.

7. Customer Concentration (Top Tenants as % of Revenue)

Definition: The percentage of total revenue contributed by the largest tenants (commonly tracked as top-5 or top-20). This measures revenue risk.

Why it matters: A REIT with high customer concentration (e.g., a large share from a single hyperscaler) faces meaningful risk if that tenant builds its own capacity or renegotiates rates. Broad tenant diversification reduces this single-point-of-failure exposure.

8. Development Yield (on Cost)

Definition: The expected stabilized NOI (Net Operating Income) from a new development divided by the total project cost. This measures the return on capital for new data center construction.

Why it matters: Construction and power-infrastructure costs have risen materially since 2020. A development yield that fails to clear the REIT's cost of capital plus a development premium signals a project that should be re-scoped or shelved. Operators generally underwrite a spread above stabilized acquisition cap rates to justify the construction risk.

9. Same-Store Revenue Growth

Definition: Year-over-year revenue growth from existing facilities that have been operational for at least 12 months. This excludes new developments and acquisitions.

Why it matters: This KPI isolates organic growth from expansion. It shows whether the REIT is effectively raising rents, increasing power utilization, or reducing churn in its stabilized portfolio. Low-to-mid single-digit same-store growth is typical; stronger figures indicate real pricing power.

10. EBITDA Margin (Adjusted)

Definition: EBITDA (Earnings Before Interest, Taxes, Depreciation, Amortization) divided by total revenue. This measures operational efficiency.

Why it matters: Data center REITs carry high fixed costs (power infrastructure, cooling, security). A high adjusted EBITDA margin indicates strong pricing power and cost control. Margins are usually reported on an adjusted basis to normalize for pass-through power revenue, which can distort the headline ratio.

Reach Kory White, Fractional CRO: 📅 Book a Quick Call · 💼 Kory on LinkedIn · 🏢 CRO Syndicate

Real Operators

Equinix (NASDAQ: EQIX)

The largest publicly traded data center REIT by market value, Equinix is built around colocation and interconnection (e.g., Equinix Fabric), which command higher margins than wholesale power leases. Its retail-heavy mix supports a relatively high adjusted EBITDA margin and low customer concentration.

Digital Realty (NYSE: DLR)

A global operator with a mix of wholesale and colocation and heavy exposure to hyperscale tenants. Digital Realty's scale and PlatformDIGITAL strategy give it large hyperscale leases alongside an interconnection business; its blended margin sits below a pure-retail operator like Equinix.

Iron Mountain (NYSE: IRM)

Better known for records storage, Iron Mountain operates a fast-growing data center segment that it reports as a distinct business. It is a useful public comparable for a diversified REIT building data center capacity alongside a legacy cash-generating business.

CyrusOne (private)

CyrusOne was a publicly traded hyperscale operator until KKR and Global Infrastructure Partners took it private in March 2022 in a roughly $15 billion transaction, after which its shares were delisted from Nasdaq. It remains a significant operator but no longer reports as a public REIT — a reminder that several large data center platforms (including QTS, taken private by Blackstone in 2021) now sit inside private capital.

American Tower (NYSE: AMT)

A communications-infrastructure REIT that expanded into data centers through its 2021 acquisition of CoreSite, giving it an interconnection-focused U.S. Colocation footprint inside a much larger tower portfolio.

Failure Modes

1. Over-Leasing Power Capacity Without Utilization Terms

Signing tenants for more power than they ramp into, without terms that compensate for reserved-but-unused capacity, ties up infrastructure the REIT has already paid to build. The mitigation is reservation and ramp clauses that have tenants pay for contracted capacity on a defined schedule rather than only when consumed.

2. Ignoring Stranded Assets

Capacity built in markets where demand does not materialize becomes a stranded asset. Building well ahead of absorption in a secondary market can leave megawatts idle, dragging returns. Disciplined operators tie speculative construction to pre-leasing thresholds.

3. Misaligned Lease Terms

Locking a long fixed-rate lease in a market where power costs are rising, without escalators or power-cost pass-through, erodes margin over the life of the lease. Mature operators include escalators and power-cost pass-through clauses to protect real returns in high-cost markets such as Northern Virginia.

4. High Customer Concentration

Heavy reliance on a single hyperscaler creates existential risk if that tenant insources capacity or slows expansion. Concentration risk is one reason interconnection-rich, many-tenant colocation portfolios trade at a premium to single-tenant wholesale exposure.

Reporting Cadence

- Daily: Power utilization (PUR) and power cost tracking. Operators use building-management and DCIM tooling (e.g., Schneider Electric EcoStruxure, Vertiv) to monitor real-time power consumption.

- Weekly: Leasing pipeline updates (pre-leasing status, signed reservations and LOIs), commonly tracked in Salesforce.

- Monthly: Revenue per MW, occupancy (power and physical), churn rate, and same-store revenue growth, reported to the board and investors.

- Quarterly: Full financials (EBITDA margin, development yield, customer concentration). Public REITs file 10-Q and 10-K reports with the SEC.

- Annually: Long-term lease expiration schedules and capital expenditure plans.

30/60/90 Day Plan

First 30 Days: Audit Current Metrics

- Week 1: Pull last 12 months of data for Revenue per MW, Occupancy (power), and Churn Rate.

- Week 2: Identify top tenants and calculate Customer Concentration.

- Week 3: Run a Power Utilization Rate analysis for each facility. Flag any facility with low utilization relative to contracted capacity.

- Week 4: Present a baseline KPI dashboard to leadership using Tableau or Power BI.

Days 31–60: Fix Gaps

- Weeks 5-6: Engage tenants with low utilization. Where appropriate, structure incentives that bring forward power ramp or right-size reservations.

- Week 7: Confirm a power-cost pass-through mechanism is present in all new leases.

- Week 8: Launch a tenant-retention program (e.g., terms for multi-year renewals) to reduce churn.

Days 61–90: Optimize for Growth

- Week 9: Model Development Yield for all pipeline projects. Re-scope or pause any project that fails to clear the cost-of-capital hurdle plus a development premium.

- Week 10: Set quarterly targets for Same-Store Revenue Growth.

- Week 11: Train the sales team on selling power and expansion upgrades to existing tenants.

- Week 12: Present a 12-month revenue forecast to the board using a planning tool such as Anaplan.

FAQ

What is the difference between power occupancy and physical occupancy? Power occupancy measures the percentage of contracted megawatts leased, while physical occupancy measures square footage leased. A facility can be high on one and lower on the other when tenants are contracted for less power than the building can deliver, or are still ramping into contracted capacity.

How do I calculate Revenue per MW for a colocation facility? Divide total annual rental revenue (excluding power pass-through) by total contracted MW. For example, a facility with $10M in rent and 5 MW contracted has a Revenue per MW of $2M.

What is a good churn rate for a data center REIT? Low single digits is excellent; mid-single digits is typical; double-digit churn is a red flag that warrants investigation into pricing and service quality.

How often should I report Development Yield? Quarterly, because construction costs and pre-leasing rates change rapidly. Use a rolling 12-month view to smooth volatility.

Why is Customer Concentration dangerous? If a single tenant represents a large share of revenue and leaves or insources capacity, the REIT can lose a substantial slice of income with no quick replacement. Diversified, interconnection-rich portfolios are more resilient.

What tools do data center REITs use to track these KPIs? Common tools include Salesforce for CRM, Tableau or Power BI for dashboards, Anaplan for planning, and DCIM platforms like Schneider Electric EcoStruxure for power monitoring.