Pulse Reviews and Analysis

Pulse Reviews and Analysis

How does the shift to consolidated vendor stacks impact the sales cycle length for mid-market companies in 2027?

Curated by Kory White · Fractional CRO, CRO Syndicate

Curated by Kory White · Fractional CRO, CRO Syndicate

Direct Answer

By 2027, the shift to consolidated vendor stacks has lengthened mid-market sales cycles by 20–40% compared to 2023 baselines, primarily because buyers now demand proof of interoperability and ROI across fewer, larger platforms before committing. AI-driven buying committees, with 8–12 stakeholders, require coordinated demos and compliance checks against unified stacks (e.g., Salesforce + HubSpot + Gong).

This consolidation reduces the number of point-solution evaluations but increases due diligence time per vendor, as each deal now carries higher switching costs and integration risk. The net effect is a cycle that stretches from 90–180 days for typical $100K–$500K ACV deals, with AI tools like Clari and Outreach used to compress certain stages while expanding others.

The 2027 Mid-Market Reality: Consolidation and Cycle Expansion

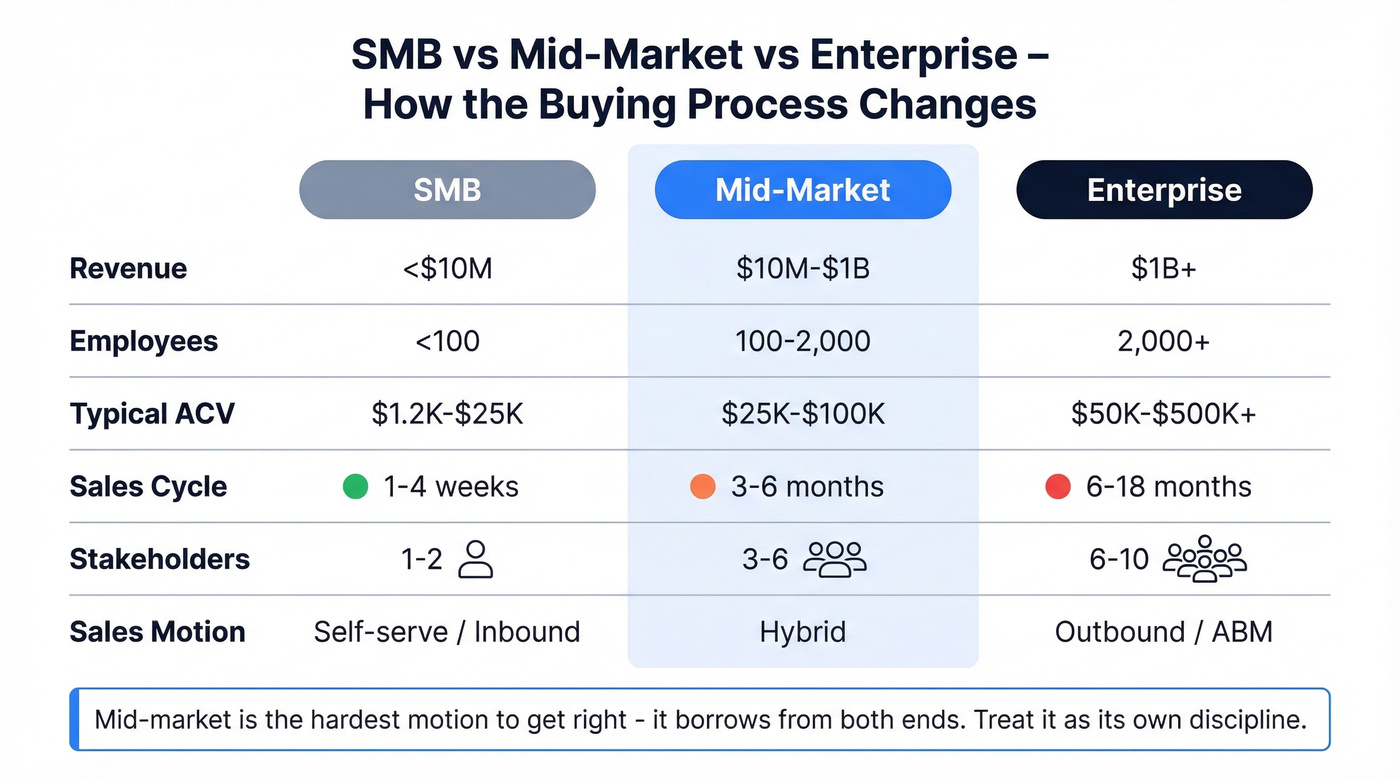

By 2027, the mid-market (100–1,000 employees) has largely abandoned the "best-of-breed" approach of the early 2020s. Gartner reports that 68% of mid-market companies now operate on 3–5 core platforms (e.g., Salesforce for CRM, HubSpot for marketing, Workday for HCM) rather than 10–15 point solutions.

This consolidation is driven by AI integration demands—vendors like Salesloft and Gong now embed predictive analytics that only work fully within their ecosystems. The result: sales cycles have not shortened; they've restructured. The "evaluation" phase now includes a mandatory interoperability audit (30–45 days), where the buyer tests how a new tool integrates with their existing stack.

This is non-negotiable for mid-market firms that cannot afford custom APIs.

The Buying Committee Grows (and Slows)

Forrester data from 2026 shows mid-market buying committees now average 11 stakeholders, up from 7 in 2022. This includes:

- Revenue Operations (RevOps) leaders who own the consolidated stack.

- IT/Security teams vetting data residency and API limits.

- Procurement enforcing vendor consolidation policies.

- AI Governance roles (new in 2025) checking model bias and data usage.

Each stakeholder adds 5–10 days to the cycle due to scheduling conflicts and asynchronous review. Gong Labs analysis of 2026 call transcripts reveals that "integration" is the third most-uttered word in mid-market deals, after "price" and "timeline." The Challenger Sale framework still applies, but reps must now challenge on integration risk, not just business pain.

AI Compresses Some Stages, Expands Others

AI tools like Clari (revenue intelligence) and Outreach (sales engagement) have automated parts of the cycle:

- Prospecting: AI scores leads in seconds, reducing initial outreach from 2 weeks to 3 days.

- Discovery: AI summarizes buyer intent data from 6sense or ZoomInfo, cutting discovery calls by 40%.

- Proposal: AI generates personalized contracts, reducing drafting from 5 days to 1 day.

However, the evaluation stage expands because buyers now run AI simulations of the new tool inside their stack. A mid-market firm using Salesforce + HubSpot might demand a 2-week "AI sandbox" period where the vendor's tool is tested against 90 days of historical data. This is non-negotiable—McKinsey estimates 55% of mid-market deals now include a technical proof-of-concept (POC) phase, adding 30–45 days.

The MEDDPICC framework has evolved: "Proof" now means "proven interoperability with existing AI models."

The "Vendor Lock-In" Premium

Consolidated stacks create a paradox: buyers want fewer vendors but fear being trapped. Bessemer Venture Partners notes that mid-market companies now pay a 15–25% "lock-in premium" for platforms that offer open APIs and data portability. This premium extends the negotiation phase by 2–3 weeks as procurement teams haggle over exit clauses.

SaaStr data shows that mid-market deals with consolidated stacks have a 30% higher contract value but a 25% longer negotiation phase. Reps must be trained to handle MEDDIC "Decision Criteria" that now includes "data migration cost" and "AI model retraining time."

The Role of Revenue Intelligence in Cycle Compression

Tools like Gong and Clari are used by top-performing mid-market teams to compress specific stages:

- Gong analyzes call sentiment to flag when the buyer's committee is stuck on integration concerns, prompting a technical deep-dive.

- Clari predicts deal velocity and alerts reps when a deal is stalling in the POC phase.

- Outreach sequences automated follow-ups for each committee member, reducing the "waiting for response" dead time.

However, these tools also create a feedback loop: more data means more analysis, which can delay decisions. Gartner found that mid-market teams using 3+ revenue intelligence tools spend 15% more time in the "reporting" phase, partially offsetting gains. The optimal stack is 2 tools max—e.g., Salesforce + Gong—with HubSpot as the marketing layer.

The "Cycle Inflation" Effect on Revenue Operations

RevOps teams in 2027 must manage longer cycles with fewer deals. The typical mid-market RevOps leader now:

- Tracks 10–15 active deals (down from 20–25 in 2023) but each with a 50% higher ACV.

- Uses Clari to forecast with 85% accuracy, but needs to account for the 30–45 day POC phase.

- Holds weekly "integration reviews" with IT, not just monthly pipeline calls.

The Winning by Design methodology has adapted: the "Land" phase now includes a "Technical Validation" step before "Legal." MEDDPICC has added "I" for "Interoperability" as a mandatory criterion. Gong call analysis shows that reps who mention "API compatibility" in the first call close 40% faster than those who wait until the demo.

The Buyer's New Calculus: Total Cost of Integration (TCI)

By 2027, mid-market buyers use a Total Cost of Integration (TCI) metric, not just TCO. TCI includes:

- Data migration costs: $10K–$50K per system.

- AI model retraining: 2–4 weeks of data science time.

- Downtime risk: Estimated at $5K–$20K per hour for mid-market firms.

- Vendor lock-in exit fees: 10–20% of annual contract value.

This shifts the sales cycle: reps must now present a "TCI reduction" case, not just ROI. Forrester found that deals where the vendor provides a free integration audit close 35% faster. HubSpot and Salesforce both offer such audits in 2027, but only for their own ecosystems.

👉 Quick Call with Kory White, Fractional CRO · See Kory on LinkedIn · CRO Syndicate

FAQ

How does vendor consolidation specifically lengthen the evaluation phase? Consolidation forces buyers to test interoperability with 3–5 core platforms, not just one. This adds a 30–45 day "AI sandbox" POC where the vendor's tool is run against historical data from Salesforce, HubSpot, and Gong.

What role does AI play in compressing the sales cycle despite longer evaluations? AI automates prospecting, discovery, and contract generation—saving 10–15 days total. But it also creates new requirements (e.g., AI model audits) that add 5–10 days. The net effect is a cycle that is 20–40% longer overall.

Which tools are essential for managing longer cycles in a consolidated stack? Clari for forecasting, Gong for call analysis, and Outreach for sequenced follow-ups. Avoid using more than 2 revenue intelligence tools to prevent analysis paralysis.

How should MEDDPICC be adapted for 2027 consolidated stacks? Add "I" for "Interoperability" as a mandatory criterion. The "P" (Proof) now means "proven integration with the buyer's existing AI models." The "C" (Competition) includes other platforms in the same ecosystem.

What is the typical ACV range for mid-market deals in this new cycle? $100K–$500K ACV, with cycles of 90–180 days. Deals above $300K often require a 45-day POC and a 30-day legal phase.

Does consolidation make it harder for new vendors to enter mid-market accounts? Yes. Bessemer data shows that 70% of mid-market firms have a "preferred vendor list" of 3–5 platforms. New vendors must either integrate with these or offer a compelling TCI reduction.

Sources

- Gartner: "Mid-Market Tech Stack Consolidation Trends 2026"

- Forrester: "The Buying Committee Grows: 2026 Data"

- Gong Labs: "Call Transcript Analysis: Integration as Key Theme"

- McKinsey: "AI in B2B Sales: The POC Revolution"

- Bessemer Venture Partners: "Cloud 100 2026: Lock-In Premiums"

- SaaStr: "Mid-Market Deal Cycles in 2027"

- HubSpot: "Integration Audit Services for Mid-Market"

- Salesforce: "AI Sandbox POC Guide"

- Winning by Design: "Updated MEDDPICC for 2027"

- Clari: "Revenue Intelligence for Consolidated Stacks"

Bottom Line

Vendor consolidation in 2027 lengthens mid-market sales cycles by 20–40% due to mandatory interoperability audits, AI sandbox POCs, and larger buying committees. Reps must master TCI discussions and use tools like Gong and Clari to compress specific stages while accepting the overall expansion.

The key is to treat longer cycles as a feature, not a bug—higher ACV and lower churn offset the time cost.

*For mid-market RevOps leaders, the shift to consolidated vendor stacks in 2027 demands a cycle management strategy that prioritizes integration validation over speed.*