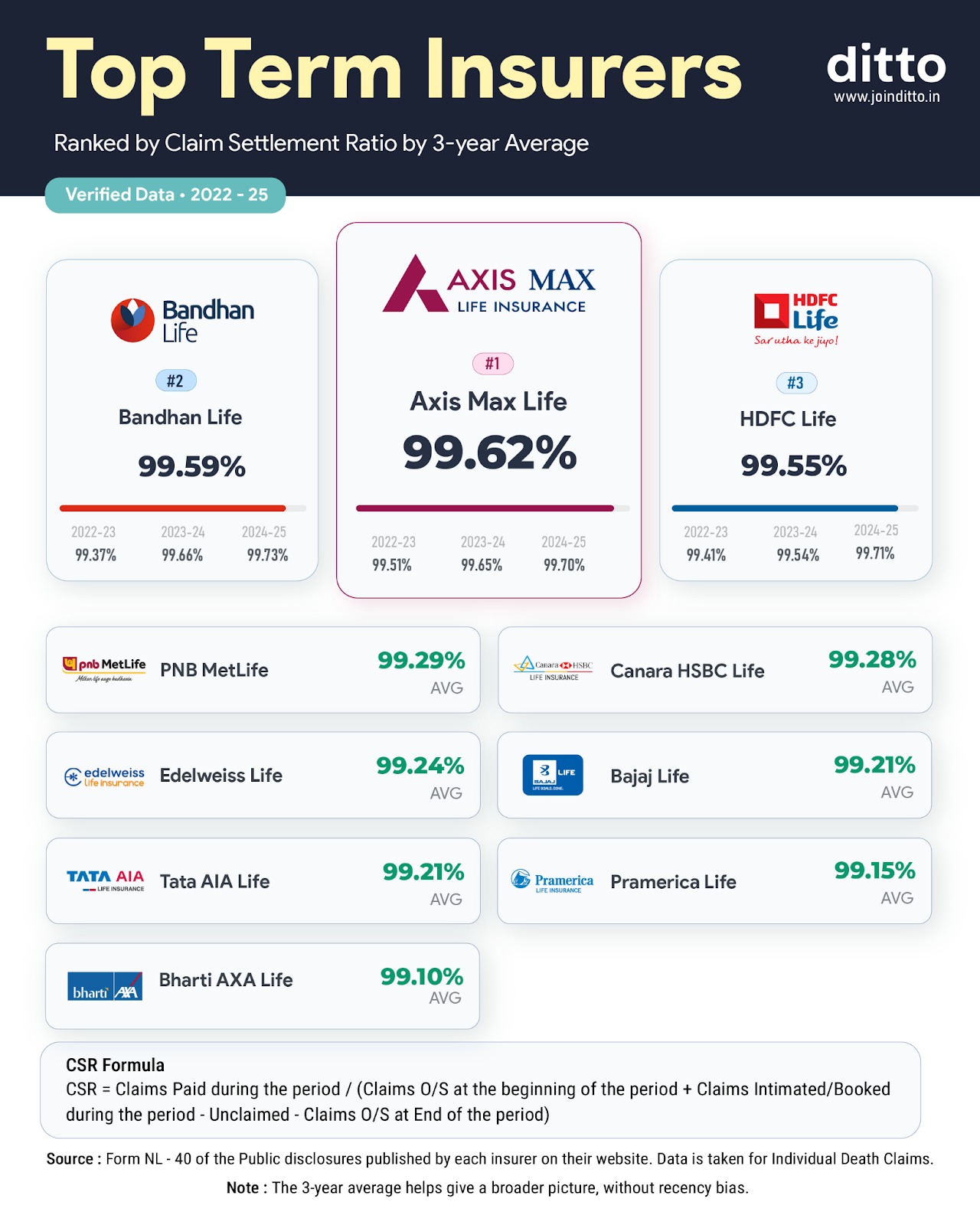

Top 10 Life Insurance Carrier Revenue KPIs

Curated by Kory White · Fractional CRO, CRO Syndicate

Curated by Kory White · Fractional CRO, CRO Syndicate

Direct Answer

Why Life Insurance Measures Differently

Life insurance carriers operate on a fundamentally different economic model than property & casualty (P&C) or health insurers. The revenue stream is not a single premium; it is a stream of premiums, often spanning decades, combined with investment returns on the float. This creates distinct measurement challenges.

First, revenue recognition is deferred. A term life policy might generate a $1,000 annual premium, but the carrier must reserve for the death benefit over 20-30 years. This means top-line revenue (premiums written) is not the same as economic profit. Carriers use Statutory Accounting Principles (SAP) for regulators and GAAP for investors, which can show wildly different results for the same block of business.

Second, investment income is a core revenue component. For a typical whole life or universal life policy, the investment spread (what the carrier earns on reserves minus what it credits to policyholders) can account for 40-60% of total profitability. This is why carriers are sensitive to interest rate changes and asset-liability matching.

Third, persistency (policy retention) is a revenue multiplier. A 1% improvement in persistency for a 30-year block of business can increase the present value of future profits by 10-15% (industry estimate). Conversely, a spike in lapses destroys future revenue streams and can trigger adverse selection (healthy policyholders leave, sick ones stay).

Finally, mortality and morbidity risk creates a direct revenue cost. Unlike P&C where claims are mostly random, life insurance claims are actuarially predictable in aggregate, but a pandemic or medical breakthrough can swing results by 20-30% in a given year.

These differences mean standard SaaS or P&C KPIs (like Monthly Recurring Revenue or Loss Ratio) are insufficient. Carriers must use actuarial metrics that discount future cash flows.

The Most Important KPIs to Track

1. New Annualized Premium (NAP)

NAP measures the total annualized premium from new policies sold in a period. It is the life insurance equivalent of "new bookings" in SaaS. It strips out single-premium policies (like some annuities) to show recurring revenue potential.

- Calculation: Sum of (First-Year Premium * Payment Frequency Factor). For monthly pay, multiply by 12.

- Benchmark: A top-quartile carrier like Northwestern Mutual or MassMutual targets NAP growth of 5-10% annually in a stable market. Prudential Financial reported $4.2B in individual life NAP for 2023 (actual figure).

- Why it matters: NAP is the leading indicator of future premium revenue. If NAP declines, the carrier is shrinking its book of business.

2. Policy Persistency (13th Month, 25th Month, 61st Month)

Persistency measures the percentage of policies still in force after a given period. It is the life insurance version of net revenue retention.

- Calculation: (Policies in force at end of period) / (Policies in force at start of period + new policies issued). Usually tracked at 13 months (after the first-year lapse spike), 25 months, and 61 months.

- Benchmark: Industry average 13-month persistency is around 85-88% for term life. Top carriers like Guardian Life achieve 90-93%. A 5-point drop in persistency can reduce embedded value by 15-20%.

- Why it matters: Lapses are the single biggest destroyer of life insurance revenue. A policy that lapses in year 2 has already cost the carrier acquisition expense (commissions, underwriting) but generated minimal premium.

3. Lapse Rate (Morbidity/Mortality Adjusted)

The raw percentage of policies terminated by the policyholder (not by death). This is distinct from mortality claims.

- Calculation: (Number of policies lapsed in period) / (Average number of policies in force).

- Benchmark: Annual lapse rates for term life range from 4-8% after year 2. For whole life, it is lower (2-4%) due to cash value accumulation. A carrier with a lapse rate above 10% on term products is likely mispricing or has poor distribution.

- Why it matters: Lapses trigger anti-selection—the healthiest policyholders are most likely to lapse, leaving a sicker, more expensive block. This directly increases the mortality margin required.

4. Mortality/Morbidity Margin

The difference between actual death claims (or morbidity claims for disability/critical illness) and the expected claims priced into the premium. This is the core underwriting profit.

- Calculation: (Expected Claims – Actual Claims) / Earned Premium. Expressed as a percentage.

- Benchmark: A well-managed block of term life should have a mortality margin of 5-15%. A margin below 5% suggests underpricing or adverse selection. RGA (Reinsurance Group of America) publishes industry mortality studies showing margins vary by age band and product.

- Why it matters: This is the "gross profit" of the insurance risk. If this margin turns negative, the carrier is losing money on every policy before expenses and investment income.

5. Investment Yield (Net Investment Income / Invested Assets)

The total return on the carrier's general account assets (bonds, mortgages, equities, alternatives). Life insurers are the largest institutional investors in corporate bonds.

- Calculation: (Net Investment Income – Investment Expenses) / Average Invested Assets.

- Benchmark: For a large mutual like New York Life, net yield is typically 4.5-5.5% in a normal rate environment. In 2023, MetLife reported a net investment yield of 4.8% on its general account.

- Why it matters: For participating whole life policies, the dividend scale is directly tied to investment yield. A 50-basis-point drop in yield can force a dividend cut, triggering lapses.

6. Combined Ratio (Life)

Adapted from P&C, this ratio measures total claims + expenses as a percentage of earned premium. For life, it is often called the Expense & Mortality Ratio.

- Calculation: (Claims + Underwriting Expenses + Commissions) / Earned Premium.

- Benchmark: A combined ratio below 100% indicates underwriting profit. Most life carriers target 85-95%. A ratio above 100% means the carrier is relying entirely on investment income for profit.

- Why it matters: This is a simple "are we making money on insurance?" check. Aflac (supplemental health/life) reported a combined ratio of 92% in 2023.

7. Expense Ratio (General Expenses / Direct Premiums Written)

The percentage of premium consumed by operating costs (excluding claims and commissions).

- Calculation: (Salaries, IT, Rent, Marketing) / Direct Premiums Written.

- Benchmark: Industry average is 20-30% for individual life. Direct-to-consumer carriers like Ladder or Ethos (using digital distribution) can achieve 15-20%. Traditional agency carriers are 25-35%.

- Why it matters: High expense ratios directly erode the margin available for policyholder dividends or shareholder returns. Voya Financial targets an expense ratio below 22%.

8. Embedded Value (EV)

The present value of future profits from the in-force block of business, plus adjusted net worth. This is the life insurance equivalent of ARR + net cash.

- Calculation: (Present Value of Future Premiums – Present Value of Future Claims & Expenses) + Free Surplus. Discount rate is typically 10-12% for European carriers, 8-10% for US mutuals.

- Benchmark: AIA Group (Asia) reported an EV of $68B in 2023. MetLife reports a similar metric called "Adjusted Book Value."

- Why it matters: EV is the single best measure of a carrier's long-term value creation. It captures the "unearned revenue" embedded in the policy block.

9. Customer Lifetime Value (CLV)

The net present value of all future profits from a single policyholder relationship, including cross-sells (e.g., adding a term rider to a whole life policy).

- Calculation: (Average Premium * Persistency * Margin) – Acquisition Cost, discounted over expected policy life.

- Benchmark: For a typical $500,000 term life policy sold to a 35-year-old, CLV is roughly $1,500-$3,000 (industry estimate). For a whole life policy with cash value accumulation, CLV can be $5,000-$15,000.

- Why it matters: CLV helps carriers decide how much to spend on acquisition. If CLV is $2,000, spending $1,500 on a commission is acceptable.

10. Net Promoter Score (NPS) – Policyholder Experience

While not strictly a revenue KPI, NPS is a leading indicator of persistency and cross-sell success. Life insurance has notoriously low NPS (industry average is 30-40, vs. 70+ for USAA or Amazon).

- Calculation: Standard NPS survey: "How likely are you to recommend [Carrier] to a friend?" (0-10).

- Benchmark: Northwestern Mutual scores around 65-70. State Farm is around 50. A carrier below 30 has a persistency problem.

- Why it matters: A 10-point NPS improvement correlates with a 3-5% improvement in 13-month persistency (internal carrier studies).

👉 Quick Call with Kory White, Fractional CRO · See Kory on LinkedIn · CRO Syndicate

Real Operators

- Northwestern Mutual: The largest US life insurer by assets. They track NAP growth and persistency obsessively. Their field force of 7,500+ advisors is compensated heavily on policy persistency (trailing commissions). They use Salesforce for CRM and Gong for call coaching to improve policyholder engagement.

- MetLife: The largest publicly traded US life insurer. They use Clari for revenue forecasting across their group benefits and individual life lines. Their investor relations materials (metlife.com) show detailed EV and combined ratio disclosures.

- Aflac: Dominates the supplemental health/life market in Japan and US. They track expense ratio and combined ratio closely. They use Workday for financial planning and Tableau for KPI dashboards.

- Ladder: A digital-native term life carrier. They use HubSpot for marketing automation and Outreach for sales engagement. Their KPI focus is on customer acquisition cost (CAC) and CLV, with a target CAC of $200-$400 per policy.

- Ethos: A digital life insurance platform backed by Sequoia Capital. They use Salesloft for lead management and Segment for data pipeline. Their KPI is "time to issue" (policy issuance in under 10 minutes is a differentiator).

Failure Modes

- Persistency Blindness: A carrier that only tracks NAP growth but ignores persistency will see revenue grow initially, then collapse as lapses accelerate. Example: A carrier that relaxed underwriting to boost sales in 2020 saw 13-month persistency drop from 88% to 78%, destroying $100M+ in embedded value.

- Misaligned Commission Structures: Paying high first-year commissions with no trailing compensation incentivizes agents to churn policies. Result: High NAP, low EV. The carrier books revenue but loses money on acquisition.

- Investment Yield Obsession: Chasing yield by buying risky assets (e.g., long-duration BBB bonds) can generate short-term investment income but creates asset-liability mismatch. Example: A carrier that loaded up on 30-year corporate bonds in 2021 saw market value drop 20% in 2022 when rates rose.

- Underpricing for Market Share: Using aggressive mortality assumptions to undercut competitors. Result: Low NAP growth but negative mortality margin. The carrier writes business that will never be profitable.

- Ignoring Digital Distribution Costs: A carrier that builds a direct-to-consumer channel but fails to track CAC by channel will overspend. Example: A carrier spending $800 CAC on a $1,000 CLV policy is losing money.

Reporting Cadence

- Daily/Weekly: NAP (new sales), Lapse Rate (early warning). Tracked in Salesforce or HubSpot dashboards.

- Monthly: Expense Ratio, Combined Ratio, Investment Yield (preliminary). Reported to CFO.

- Quarterly: Persistency (13-month, 25-month), Mortality Margin, Embedded Value (full actuarial run). Presented to Board.

- Annually: Full EV calculation, CLV by cohort, NPS survey. Used for strategic planning and capital allocation.

Tool Stack: Clari for revenue forecasting, Tableau or Power BI for KPI dashboards, Workday Adaptive Planning for financial modeling.

30-60-90

First 30 Days: Audit & Baseline

- Gather 12 months of NAP, persistency, and expense ratio data.

- Identify the top 3 KPIs that are below industry benchmark (e.g., 13-month persistency below 85%).

- Review commission structure for misalignment with persistency.

- Set up a Tableau dashboard with daily NAP and weekly lapse rate.

Days 31-60: Fix Leaks

- Implement a persistency improvement program: automated policyholder outreach using Outreach sequences for policies approaching lapse.

- Adjust underwriting guidelines if mortality margin is below 5%.

- Rebalance investment portfolio if yield is below 4.5% or duration mismatch exceeds 2 years.

- Run a CLV analysis by distribution channel (agent vs. Digital). Kill low-CLV channels.

Days 61-90: Optimize & Scale

- Launch a cross-sell campaign targeting high-CLV policyholders (e.g., offering term riders to whole life holders).

- Set quarterly EV targets for each product line.

- Implement a Gong-powered call review to improve agent persistency messaging.

- Present a 12-month KPI improvement plan to the Board, with specific targets (e.g., improve 13-month persistency from 85% to 88%).

FAQ

? What is the difference between NAP and total premium? NAP strips out single-premium policies and focuses on annualized recurring premium. Total premium includes all cash received, which can be distorted by large single-pay policies.

? How often should I calculate Embedded Value? Annually for full actuarial calculations. Quarterly for a simplified update using a standardized discount rate.

? Why is persistency more important than NAP for mature carriers? For a carrier with $10B in in-force premium, a 1% improvement in persistency adds $100M in retained premium. That is often more valuable than a 10% NAP growth on a $500M new business base.

? What is a healthy combined ratio for a life carrier? Below 95% is excellent. 95-100% is average. Above 100% means the carrier is losing money on insurance risk and relying on investment income.

? How do I track CLV for a 30-year term policy? Use a discounted cash flow model with a 10-12% discount rate. Assume a lapse curve (e.g., 10% in year 1, 5% in years 2-5, 3% thereafter). Include expected cross-sell revenue.

? What tools do top carriers use for KPI tracking? Clari for revenue forecasting, Tableau for dashboards, Workday for financial planning, Salesforce for CRM, and Gong for sales analytics.

? How does investment yield affect policyholder dividends? For mutual carriers, a 50-basis-point drop in yield typically reduces the dividend scale by 10-20%. This can trigger lapses.

? What is the biggest mistake carriers make with KPIs? Focusing only on top-line growth (NAP) and ignoring persistency and mortality margin. This leads to writing unprofitable business.

Sources

- NAIC: Life Insurance Industry Data

- MetLife 2023 Annual Report (Investor Relations)

- Northwestern Mutual Financial Highlights

- Aflac 2023 Annual Report (Combined Ratio Data)

- RGA: Mortality & Morbidity Studies

- Gartner: Insurance KPI Benchmarking

- Salesforce: Life Insurance CRM Solutions

- Clari: Revenue Intelligence for Insurance