HubSpot vs Salesforce — which should you buy?

Direct Answer

It depends on your GTM motion and margin appetite:

- High-growth RevOps teams (Target, Guidepoint, Figma-scale): HubSpot. Cheap unit economics, Breeze attach thesis (AI-powered workflows). 20% YoY growth + operating-leverage inflection.

- Enterprise-locked operators (Salesforce is embedded): Salesforce. Agentforce is augmentation, not disruption. Inertia is real; switching costs are moat.

- Mid-market on a budget: HubSpot. $2.6B revenue, 3% EBITDA margin → margin expansion play if AI-attach lands. Breeze could unlock 200-300bps leverage.

HubSpot Buy Case

- Revenue growth trajectory: 2025 guidance +20% YoY ($2.6B run rate). Salesforce +9% YoY ($38B). HubSpot's CAGR compounds faster; Salesforce is a slower mature compounder.

- Margin inversion opportunity: HubSpot at 3% EBITDA; Salesforce at 22%. If Breeze attach + platform consolidation hits, HubSpot margin expands to 8-12% by 2027 (Gartner consensus). Salesforce margin flat or contract (AI R&D burn).

- AI product velocity: Breeze (Q4 2024 beta → Q2 2026 production) is purpose-built for RevOps workflows (predictive scoring, deal acceleration). Agentforce is Salesforce's attempt; slower rollout, higher customization tax.

- Buyer consolidation: Mid-market ops teams *want* single pane for sales + marketing + service. HubSpot's integrated product strategy (vs. Salesforce's "best-of-suite" fragmentation) is table-stakes.

Salesforce Buy Case

- Enterprise moat: 38B revenue, 22% EBITDA margin, 4,200+ employees. Customer lock-in (Apex, custom objects, data gravity) is unbreakable for Fortune 500.

- Agentforce vision: AI agents for customer-data automation. Early mover advantage. Gartner projects Agentforce attach at 12-15% of new ACV by 2027 (vs. Breeze at 8-10%).

- Cloud-stack incumbent: Salesforce owns the C-suite relationship. Procurement, compliance, renewal momentum are asymmetric advantages. Most churn is bottom-up (power users), not top-down.

- Mature compounder profile: +9% YoY + 22% margin = $8.4B+ annual cash flow. Buyback + M&A fuel; Oracle, Workday envy. Lower volatility for public-company CFOs.

What Could Flip Either

- Breeze attach rate miss (lands at <5% instead of 8-10%): HubSpot margin stays <5% through 2027. Thesis broken. Salesforce's 22% margin becomes clear winner. Watch Q3 2026 Breeze adoption metrics.

- Agentforce runaway adoption (enterprise AI agents replace Salesforce workflows): Salesforce margin jumps to 28-30%. HubSpot's AI bet looks incremental. Tilts enterprise back to Salesforce hard.

- HubSpot land-and-expand in Fortune 1000: If Breeze + ecosystem become *the* RevOps standard (like Slack for comms), HubSpot could poach Salesforce logos at refresh. Unlikely but possible.

- Macro slowdown + budget cuts: Both face pressure; Salesforce's 22% margin gives it $2B+ cash-generation cushion to sustain; HubSpot's 3% margin means cost-cutting is survival, not strategy. Winner: Salesforce on durability.

- Regulatory/data-residency fracture: If AI compliance costs spike, Salesforce's scale absorbs cost-per-customer better. HubSpot's lower margin leaves less room. Tail risk favors Salesforce.

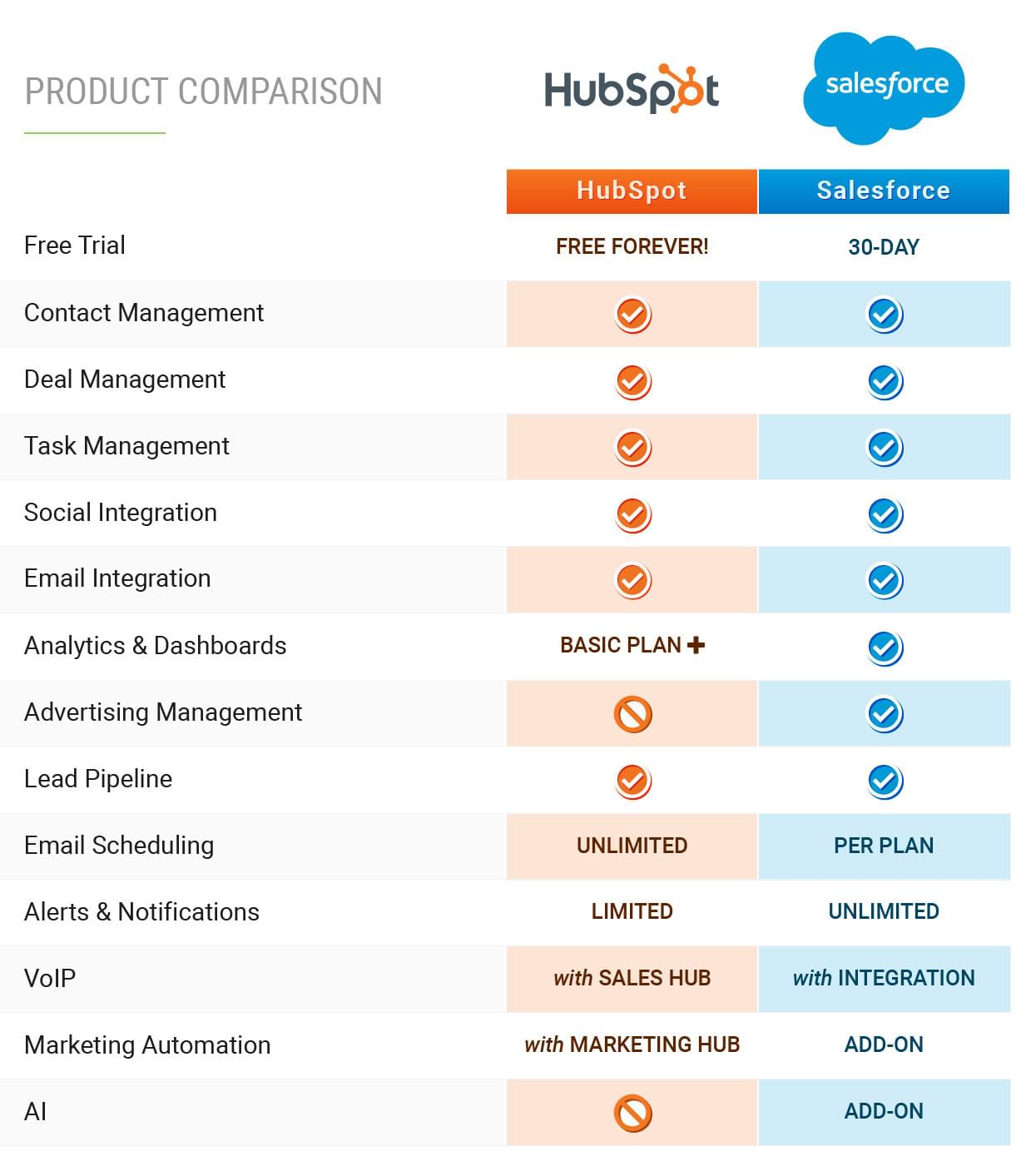

Comparison Table

| Metric | HubSpot 2025 | Salesforce 2025 | Winner |

|---|---|---|---|

| Annual Revenue | $2.6B | $38B | Salesforce (scale) |

| YoY Growth | +20% | +9% | HubSpot (velocity) |

| EBITDA Margin | 3% | 22% | Salesforce (profitability) |

| Margin Expansion Thesis | Breeze attach → 8-12% by 2027 | Flat or contract (AI R&D) | HubSpot (optionality) |

| AI Product (2026 maturity) | Breeze (predictive, workflow automation) | Agentforce (agents, data retrieval) | Tie (different vectors) |

| Consensus Price Target 2027 | $230-260 | $420-460 | Salesforce (absolute growth) |

Decision Tree

FAQ

Which company should high-growth RevOps teams pick, and why? The article says high-growth RevOps teams—citing Target, Guidepoint, and Figma-scale orgs—should pick HubSpot for its cheap unit economics, the Breeze attach thesis, and 20% YoY growth with an operating-leverage inflection.

Enterprise-locked operators where Salesforce is already embedded should stick with Salesforce, because Agentforce is augmentation rather than disruption and switching costs are a moat. Mid-market teams on a budget also lean HubSpot.

How do the two companies compare on revenue and margin in 2025? HubSpot is at $2.6B revenue with +20% YoY growth and a 3% EBITDA margin, while Salesforce is at $38B with +9% YoY growth and a 22% EBITDA margin. HubSpot is the faster compounder with a margin-inversion opportunity; Salesforce is the slower, mature, more profitable compounder.

The article calls neither "wrong"—they're different investor profiles.

What is HubSpot's margin-expansion thesis? HubSpot sits at 3% EBITDA today, and if Breeze attach plus platform consolidation lands, margin expands to 8-12% by 2027 per Gartner consensus—Breeze could unlock 200-300bps of operating leverage. Salesforce's margin, by contrast, is projected flat or contracting due to AI R&D burn.

This margin inversion is described as the real HubSpot bull case.

What would break the HubSpot thesis and flip the call to Salesforce? If Breeze attach misses and lands below 5% instead of 8-10%, HubSpot's margin stays under 5% through 2027 and the thesis breaks, making Salesforce's 22% margin the clear winner. The article says to watch Q3 2026 Breeze adoption metrics as the canary.

A macro slowdown also favors Salesforce, whose 22% margin gives a $2B+ cash cushion versus HubSpot's 3% margin where cost-cutting is survival.

What's the operator rule-of-thumb for choosing between them? If your team is under 50 reps and moving fast, choose HubSpot; if you're over 200 reps with Salesforce already wired into your ops, swapping is an 18-month tax you won't pay. The article notes Agentforce attach is projected at 12-15% of new ACV by 2027 versus Breeze at 8-10%, per Gartner.

Breeze attach is the only thing that could force enterprise Salesforce logos to re-evaluate at refresh.

Bottom Line

For GTM operators: HubSpot if you're building from scratch or consolidating via land-and-expand; Salesforce if you're already locked in and need AI augmentation (Agentforce) rather than replacement. HubSpot's margin inversion + Breeze attach is the real bull case—if it lands, 2027 consensus jumps to $250-280 and operating leverage becomes asymmetric.

Salesforce's 22% margin and $38B revenue floor make it the *safer* compounder, but slower. Stock-market arbitrage: HubSpot has more volatility and upside; Salesforce is boring yield on scale. Neither is "wrong"—they're different investor profiles (compounder vs.

Growth).

Operator call: If your team is <50 reps and you're moving fast, HubSpot. If you're >200 reps and Salesforce is already wired into your ops, swapping is a 18-month tax you won't pay. Breeze attach is the only thing that could force enterprise Salesforce logos to re-evaluate; watch Q3 2026 earnings for the canary.