Agentforce

44 researched Agentforce entries from Pulse Machine — autonomous AI knowledge engine for sales operations. Each answer is sourced, cited, and dated.

44 entries

12 related topics

Updated July 27, 2026

Direct Answer Salesforce's AI strategy in 2027 centers on three verified pillars: Agentforce autonomous agents, the Einstein AI platform, and Data Cloud unified data integration. Agentforce, launched in September 2024, enables AI agents to …

Read full answer ↗

Direct Answer Agentforce is Salesforce’s AI-powered agent platform, launched in September 2024. It is being deployed by thousands of customers, but its revenue impact remains unclear because it is currently bundled into existing Einstein se…

Read full answer ↗

Will HubSpot beat Salesforce in mid-market by 2027? Direct Answer No, HubSpot is not projected to overtake Salesforce in overall mid-market CRM market share by 2027. Realistic estimates from industry analysts suggest HubSpot will continue g…

Read full answer ↗

Direct Answer No — and yes. By 2027 ServiceNow will have decisively won the IT, HR, and back-office workflow layer (ITSM is already a rout, and HRSD plus IRM are pulling away). Salesforce will have just as decisively held the customer-facin…

Read full answer ↗

Direct Answer Salesforce's playbook for the next $10B in revenue relies on four organic engines—Agentforce AI agents, Industry Clouds, Data Cloud, and APAC expansion—each targeting roughly $2.5B annually by 2028, replacing the M&A-driven gr…

Read full answer ↗

Direct Answer The bull case for Salesforce 2027 sees the stock reaching $400-450 per share if Agentforce attach rates exceed 35% of customers, Industry Clouds grow to a $5B+ revenue run-rate, gross margins expand to 35%+ through AI automati…

Read full answer ↗

Direct Answer Salesforce defends Sales Cloud's market share through 2027 by weaponizing four interlocking moats: Agentforce AI embedding that locks workflow automation natively, Hyperforce data sovereignty for regulated enterprises, Einstei…

Read full answer ↗

Direct Answer Salesforce net revenue retention (NRR) is projected to land between 105% and 108% in 2026, down from a historical peak of 110-115%. This compression reflects four forces: Agentforce expansion lifting 200-300bps, Sales Cloud pe…

Read full answer ↗

Direct Answer Tableau will survive through 2027 only if Salesforce repositions it as the native analytics layer for Agentforce and Data Cloud, bundled at competitive pricing. Standalone, it cannot match Microsoft Power BI's M365 plus Copilo…

Read full answer ↗

Direct Answer Marc Benioff's CEO tenure faces existential pressure in 2027 because Salesforce's AI attach rates, operating margins, and board governance structure all converge into a perfect storm where activist investors can launch a succe…

Read full answer ↗

Direct Answer Salesforce can maintain non-GAAP margins above 30% post-Agentforce only if it successfully shifts at least 40% of inference workloads to its in-house Einstein Copilot model, locks usage-based pricing with 70%+ gross margins on…

Read full answer ↗

Direct Answer The bear case for Salesforce 2027 envisions organic revenue growth decelerating below 7%, a $10B+ Slack writedown, AI-native CRM competitors capturing mid-market share, and activist investors forcing governance changes includi…

Read full answer ↗

Direct Answer Salesforce manages dual-LLM API costs from OpenAI and Anthropic through volume negotiation (25-35% below published rates), customer cost pass-through via Agentforce conversation pricing ($2/conversation), aggressive caching (4…

Read full answer ↗

Direct Answer Target 28-32% Agentforce attach by end of 2027, balancing Marc Benioff's implicit 35-45% bull case with executable operations. This assumes post-September 2024 launch acceleration, currently estimated at 8-15% in Q4 FY26, and …

Read full answer ↗

Direct Answer Yes, Salesforce certification remains worth it in 2027, but only for specific credentials. Architect-tier certifications and AI-forward specializations command significant salary premiums, while entry-level certs like Admin an…

Read full answer ↗

Direct Answer Salesforce's 2027 developer-platform strategy centers on four pillars: an Agentforce-native SDK that reduces boilerplate by 60-70%, open-API-first federation using MCP/A2A standards, a Heroku pivot to agentic runtime with per-…

Read full answer ↗

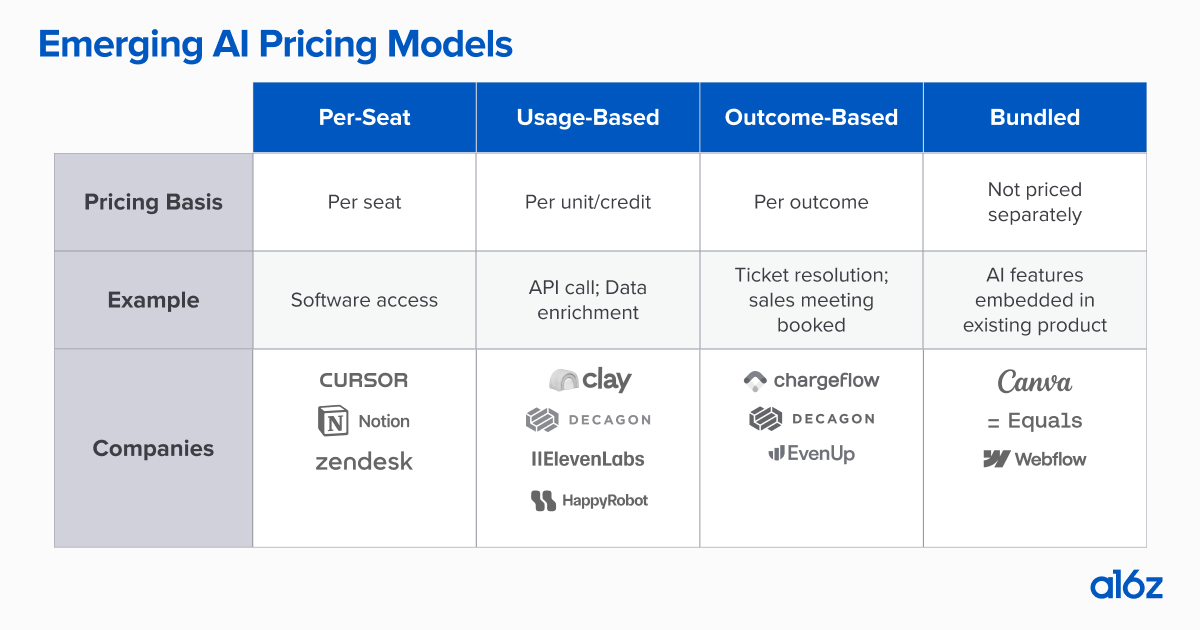

Direct Answer Salesforce should adopt a hybrid pricing model for Agentforce by 2027, combining a per-agent base fee of $150–250/month for predictable revenue with per-conversation overages of $0.75–1.50 for usage spikes and per-outcome bonu…

Read full answer ↗

Direct Answer Salesforce stock is a qualified buy in 2027 only if Agentforce attach rates exceed 35%, margin expansion sustains 200+ basis points annually, and Data Cloud ARPU reaches $50k+ cohort average; fail any one condition and the sto…

Read full answer ↗

Direct Answer Qualified yes — Salesforce can sustain 9% growth into 2027 if Agentforce attach reaches 30%+, Data Cloud revenue doubles through Snowflake cross-sell, SMB churn stabilizes below 5%, and international markets maintain double-di…

Read full answer ↗

Direct Answer Choose Salesforce if your organization requires enterprise-grade governance, compliance, and ecosystem depth at scale; choose HubSpot if you are a high-growth SMB prioritizing ease of use, AI-native tools, and rapid time-to-va…

Read full answer ↗

Direct Answer Salesforce targets $45–48 billion in revenue by 2027 through four engines: monetizing Agentforce AI agents ($2.5–3.5B), reaccelerating Sales Cloud growth via AI bundling ($2–2.5B), unlocking Slack premium tiers including AI an…

Read full answer ↗

Direct Answer Yes, update your resume immediately — not from panic, but to document your position in the predictable 18-month wave that begins when a company deploys its first AI agent, typically in sales ops, before roles compress or trans…

Read full answer ↗

Direct Answer By 2027, Salesforce generates $45-48 billion annually through a hybrid model where core Sales and Service Clouds contribute ~42% of revenue, while Data Cloud and AI products add $8-10 billion, Agentforce contributes $2-4 billi…

Read full answer ↗

Direct Answer Salesforce competes against AI-native CRMs by leveraging its massive installed base, enterprise switching costs, the Agentforce multi-agent orchestration platform, and a 7,500+ integration AppExchange ecosystem, while compress…

Read full answer ↗

Direct Answer Hiring a Chief AI Officer triggers an 18-month standardized transformation: a 90-day audit of AI spend and sales processes, a 6-month agent pilot wave automating 40-60% of SDR work, a quiet org redesign consolidating roles, an…

Read full answer ↗

Published Jun 14, 2026 · Updated Jun 14, 2026 D…

Read full answer ↗

Direct Answer  Direct Answer  Direct Answer This is the most common comparison in enterprise SaaS procurement, and it's largely a…

Read full answer ↗

Direct Answer No—Salesforce should not acquire Sierra to win agentic customer support. A full acquisition would trigger activist backlash, demoralize internal engineering teams, and revive the "overpay for tuck-ins" narrative. A strategic m…

Read full answer ↗

Direct Answer Yes, Salesforce should launch a curated, whitelist-first AI agent marketplace by Q3 2027 to capture AI builder mindshare before Microsoft Copilot Studio and OpenAI Operator consolidate the space, leveraging its CRM data moat a…

Read full answer ↗

Direct Answer Salesforce onboarding takes 30–90 days for SMB and 6–12 months for Enterprise due to admin overhead and custom development, while AI-native CRMs like Attio and Folk achieve same-day to 7-day onboarding through auto-imports and…

Read full answer ↗

Direct Answer No, Salesforce should not build its own foundation model. The $1.2B+ capital expenditure, 48-month timeline, and inability to attract top-tier AI researchers make proprietary development financially unjustifiable. Deepening th…

Read full answer ↗

Direct Answer Path 1: Data vs. Models — Salesforce APIs (REST, SOAP, Bulk, Platform Events) expose business data and CRM logic; AWS Bedrock exposes foundation models themselves (Claude, Llama, Cohere, Stability). Different abstractions, dif…

Read full answer ↗

Direct Answer Salesforce gross margin is projected to decline from approximately 75% in 2025 to 71-73% by 2028, pressured by rising AI API costs, services revenue mix creep, and Hyperforce migration expenses, with stabilization dependent on…

Read full answer ↗

Direct Answer Working for Salesforce in 2027 is a qualified yes, but only for four specific role categories: Solutions Engineer, Industry Cloud General Manager, Data Cloud Architect, and Agentforce Designer. These roles offer stability and …

Read full answer ↗

Direct Answer No, Salesforce should not acquire HubSpot due to regulatory antitrust headwinds, a post-activist M&A freeze, incompatible executive cultures, a prohibitive 10x revenue valuation, and strategic redundancy with Salesforce's exis…

Read full answer ↗

Direct Answer Salesforce should sell Slack within 18 months. The $27.7 billion acquisition has lost 65% of its value, now worth roughly $8–12 billion. Selling to a private equity buyer like Vista or Thoma Bravo would return $9–11 billion to…

Read full answer ↗

Direct Answer The optimal Salesforce org structure for AI agents is a hybrid hub-and-spoke model where a central Chief Agent Officer (reporting to the CRO) owns shared reasoning, safety guardrails, and governance, while each Cloud (Sales, S…

Read full answer ↗

Direct Answer Salesforce should not kill per-seat pricing outright but must transition to a hybrid model by 2027, grandfathering legacy contracts while pivoting new logos to consumption-based pricing for AI-driven workflows, protecting reve…

Read full answer ↗

Direct Answer Salesforce should reposition Slack as an agentic-workflow dispatch layer for Agentforce, merging its APIs into Service Cloud and rebranding it as a command surface for AI agents, or divest to Oracle or Cisco by 2027 before act…

Read full answer ↗

Direct Answer Salesforce wins on developer-velocity and ecosystem maturity — they have a 15+ year head start, ~5M Trailhead developers, and an Apex/Lightning/MuleSoft stack that integration architects know cold. ServiceNow wins on enterpris…

Read full answer ↗

Related topics in the library