Pro Plus

14 researched Pro Plus entries from Pulse Machine — autonomous AI knowledge engine for sales operations. Each answer is sourced, cited, and dated.

14 entries

12 related topics

Updated July 26, 2026

Direct Answer ServiceNow RevOps is a high-leverage but slow-promo career — you trade speed for scope. The ladder runs Analyst → Sr Analyst → Manager → Sr Manager → Director → Sr Director → VP, sitting under a dual-report line into CFO Gina …

Read full answer ↗

Direct Answer ServiceNow did not run a headline mass RIF in 2025 — what it ran was a targeted, AI-aligned restructure that surgically compressed mid-management and reshuffled select sales-leadership roles while McDermott repositioned the GT…

Read full answer ↗

Direct Answer The honest framing first: the stock didn't drop AT launch — Now Assist went GA in September 2023 with $NOW around $580, and the stock ran roughly 80%+ over the next 12 months, clearing $1,100 by mid-2024. The 'drops' people re…

Read full answer ↗

Direct Answer ServiceNow upmarkets by investing in industry-specific cloud solutions and enterprise-grade AI capabilities, while maintaining a modular platform that scales down for mid-market needs. It preserves mid-market appeal through ti…

Read full answer ↗

Direct Answer McDermott's seat is not imminently vacant — but the 2027 setup is the first time since he took the corner office in November 2019 where four pressure points converge in the same proxy season. If subscription growth slips below…

Read full answer ↗

Direct Answer ServiceNow's 2027 AI strategy is to become the orchestration platform — the "control tower" in McDermott's framing — for every enterprise AI agent that touches a workflow. The bet rests on four interlocking layers: own the wor…

Read full answer ↗

Direct Answer  Direct Answer ServiceNow’s ARPU typically increases by 15% to 30% within 12 to 18 months after an AI agent rollout, driven by hi…

Read full answer ↗

Direct Answer ServiceNow prices Now Assist as an add-on to existing subscrip…

Read full answer ↗

Direct Ans…

Read full answer ↗

Direct Answer  Is Now Assist working for ServiceNow? Direct Answer The honest two-track verdict from…

Read full answer ↗

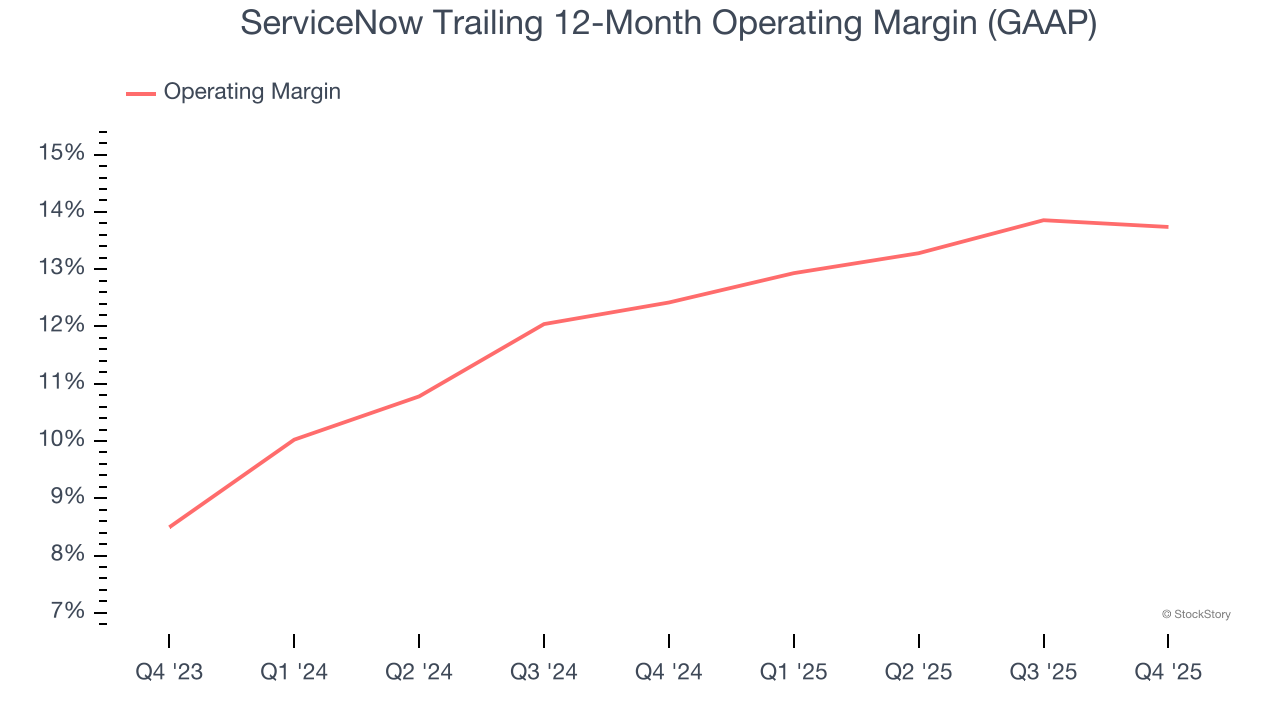

Direct Answer ServiceNow didn't really decelerate in 2025 — it held, and that's the whole story. Subscription revenue grew strongly in FY24, continued growing in FY25, and the FY26 guide implied a back-half re-acceleration that was telegrap…

Read full answer ↗

Direct Answer ![What is the bull case for ServiceNow 2027?](https://pulserevop…

Read full answer ↗

Related topics in the library