Snowflake

52 researched Snowflake entries from Pulse Machine — autonomous AI knowledge engine for sales operations. Each answer is sourced, cited, and dated.

52 entries

12 related topics

Updated July 26, 2026

Direct Answer The bull case for Snowflake 2027 targets $200+ per share through Cortex AI reaching $400M+ standalone ARR with 25%+ workload attach, net revenue retention stabilizing at 125%+ via Iceberg and Industry Cloud expansion, Polaris …

Read full answer ↗

Direct Answer Snowflake defends against open-source Iceberg data lakes by embracing the open format through Polaris Catalog, then building proprietary value layers—Cortex AI, governance, and marketplace network effects—that create switching…

Read full answer ↗

Direct Answer Qualified yes—by 2026, Snowpark has moved from beta showcase to production workload in roughly 30-40% of Snowflake's installed base, but remains constrained by Container Services adoption ceilings and ML incumbents like Databr…

Read full answer ↗

Direct Answer Yes, for Solutions Engineers, Industry Cloud Specialists, Cortex Architects, and Data Sharing Architects. No for tier-1 SDRs and generalist mid-market AEs. Snowflake in 2027 is a proven platform in deceleration — growth has sl…

Read full answer ↗

Direct Answer Snowflake stock remains a qualified buy in 2027 contingent on Cortex AI attach reaching 8-12% ARPU lift by Q3 FY27, Industry Cloud clearing $500M standalone ARR, EBITDA margins holding above 15% on $3.8B+ revenue, and Iceberg …

Read full answer ↗

Direct Answer Snowflake will survive through 2027 as an independent platform with 75-80% probability, holding its position as the vendor-neutral multi-cloud warehouse for enterprises that refuse single-cloud lock-in, despite intense pricing…

Read full answer ↗

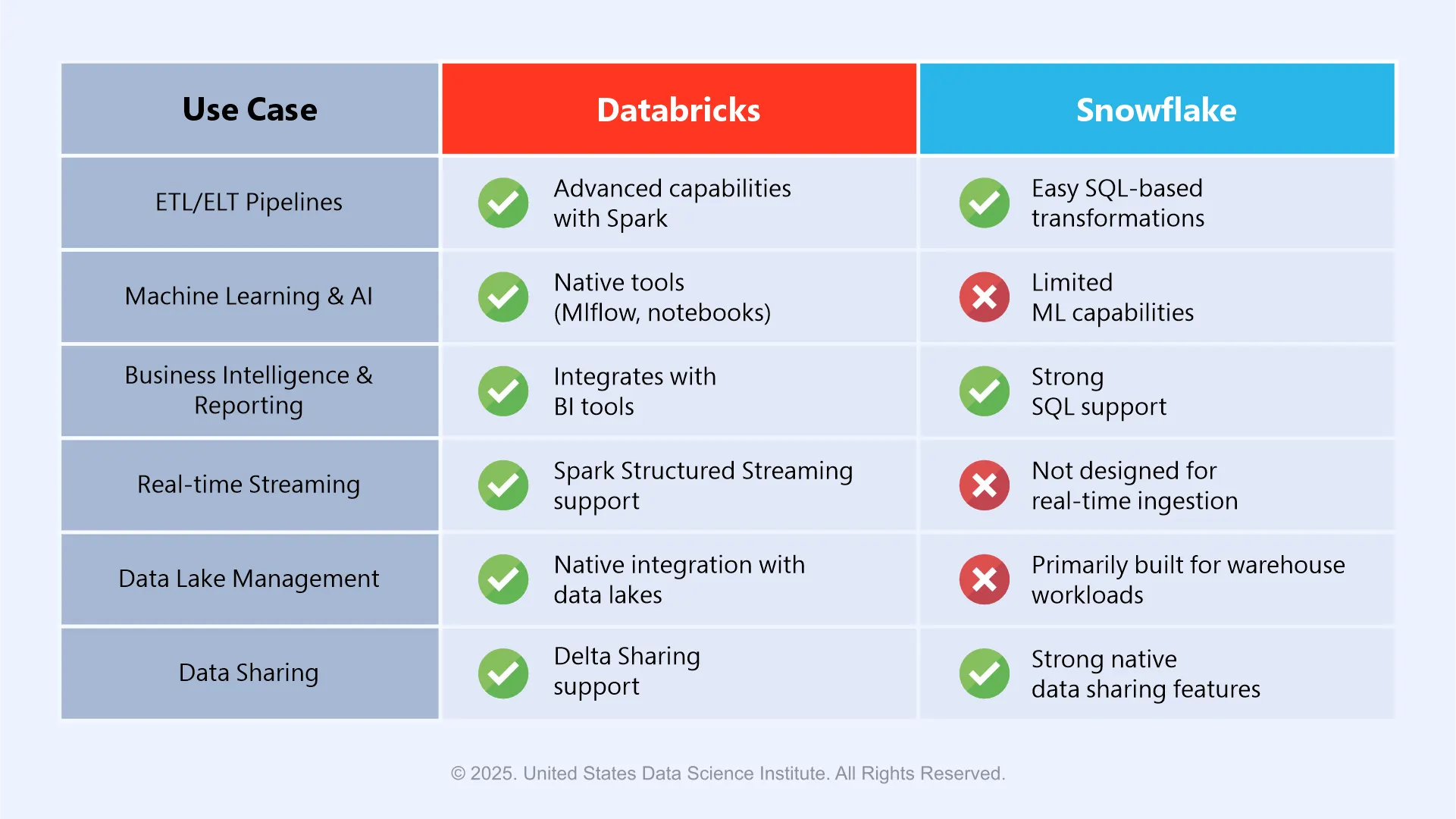

Direct Answer Snowflake onboarding is faster for SQL analytics, with first queries in ~10 minutes and no compute decisions, while Databricks wins for ML workflows, with first trained models in ~45 minutes via notebooks and MLflow — the righ…

Read full answer ↗

Direct Answer Yes, Snowflake should launch an AI agent marketplace by extending its existing Snowflake Marketplace with an agent listing type rather than building a separate storefront, leveraging the Native Apps Framework, Snowpark Contain…

Read full answer ↗

Direct Answer Snowflake's M&A strategy through 2028 follows a disciplined, three-scenario framework centered on selective tuck-in acquisitions for AI and observability through 2025-2026, with a 50% probability of one to two larger strategic…

Read full answer ↗

Direct Answer Snowflake should implement a hybrid model where the Cortex Agent Platform Lead owns agent infrastructure, safety gates, and cost governance, while Industry Cloud GMs own vertical-specific tuning, go-to-market, and ROI measurem…

Read full answer ↗

Direct Answer Snowflake should not eliminate consumption pricing entirely but must hybridize it with mandatory commit tiers, unbundled AI pricing, and outcome-based flex contracts by 2027, as pure consumption creates CFO budget risk, depres…

Read full answer ↗

Direct Answer Snowflake competes against AI-native data platforms by leveraging its enterprise-scale compute-storage separation, adopting Apache Iceberg for open-format interoperability, embedding Cortex AI for native LLM inference, and mai…

Read full answer ↗

Direct Answer Snowflake targets ~$5B in FY27 revenue (up from ~$3.5B in FY26) through four engines: Cortex AI monetization ($300-500M), Snowpark Container Services ($300-500M), Apache Iceberg open-data-lake defensive lock-in ($200-400M), an…

Read full answer ↗

Direct Answer Snowflake's net revenue retention in 2026 is projected to land in a 120-128% band, with a most likely range of 123-125%, down from 145% in 2022 but still best-in-class among data platforms, contingent on Cortex AI traction off…

Read full answer ↗

Direct Answer Snowflake's growth decelerated from 38% in FY24 to 30% in FY25 and a guided 28% in FY26 due to four structural headwinds: Apache Iceberg eroding its proprietary lock-in, AWS Redshift and Microsoft Fabric undercutting compute p…

Read full answer ↗

Direct Answer Snowflake will likely maintain 25%+ growth into 2027 only if Cortex AI inference reaches production scale with over 40% attach rate in large accounts, Iceberg cannibalization stays under 15% of net-new workloads, and the compa…

Read full answer ↗

, mid-market expansion ($0.8-1.2B), sovereign cloud and public sector ($0.6-0.9B), Mar…

Read full answer ↗

How should Snowflake price Streamlit against PowerBI? Direct Answer Kill the per-app license, lean fully into p…

Read full answer ↗

What is the right Cortex attach goal for 2027? Direct Answer A realistic Cortex attach goal for FY27 — defined as the percentage of paying Snowflake customers running at least one Cortex feature (LLM Functions, Cortex Search, Cortex Analyst…

Read full answer ↗

Direct Answer  No. …

Read full answer ↗

Direct Answer Snowflake's data-region strategy through 2027 deliberately splits across AWS, GCP, and Azure, with each hyperscaler serving a distinct role: AWS leads mature data-warehouse markets, GCP leads AI workload regions with dense GPU…

Read full answer ↗

Direct Answer Snowflake, BigQuery, and Redshift each use fundamentally different compute pricing models — credits per warehouse size, per-TB scanned, and per-node or RPU-hour respectively — so the cheapest option depends entirely on workloa…

Read full answer ↗

Direct Answer Snowflake's churn math under AI pressure decomposes into three distinct buckets—logo churn, downsell/optimization, and consumption-shrink—with net revenue retention (NRR) projected to settle in the 110-125% range by FY28 depen…

Read full answer ↗

Direct Answer Yes, Snowflake should launch vertical-data sub-brands for Healthcare & Life Sciences and Financial Services by mid-2027, as these two industries possess sufficient anchor-customer density, compliance requirements, and partner …

Read full answer ↗

Direct Answer Snowflake defends its Marketplace partners through a four-lever strategy: Native App Framework lock-in that eliminates data egress, co-sell economics with named rep splits and MDF, exclusive Cortex AI agent integration, and cu…

Read full answer ↗

Direct Answer Snowflake's product gross margin is on a trajectory to …

Read full answer ↗

Is Snowflake certification worth it in 2027? Direct Answer It depends on your role, and the dollar math is uneven. Data Engineers and Architects: YES — SnowPro Advanced is a measurable resume filter at many large enterprises and consultanci…

Read full answer ↗

What is Snowflake RevOps career path in 2027? Direct Answer The Snowflake RevOps ladder runs…

Read full answer ↗

Direct Answer A Snowflake AE role in 2027 is a conditional yes — viable only if you secure an Enterprise, Strategic, or Public Sector seat with a written Cortex AI carve-out and treat it as a 24-month resume-and-network accelerator, not a m…

Read full answer ↗

Direct Answer Snowflake faces retention challenges as consumption-pricing quota inflation, AI-native startup …

Read full answer ↗

What is the bear case for Snowflake 2027? Direct Answer Snowflake trades at a premium valuation today. The bear case compress…

Read full answer ↗

Direct Answer Snowflake should not acquire Fivetran outright. Instead, Snowflake should acquire Estuary for $2.5–3.5B to secure an open-source ingestion moat, then formalize a preferred partnership with Fivetran. This avoids ecosystem backl…

Read full answer ↗

Direct Answer Snowflake should acquire Census, not Hightouch, for an estimated $350–450 million. Census offers tighter product-market fit in operational activation for Salesforce and HubSpot, lower integration friction, and immediate defens…

Read full answer ↗

Direct Answer Yes, conditionally: Snowflake is winning mid-market customer count but struggling on unit economics. Standard Edition captured 35-40% of new ARR, yet average ACV sits at $80K versus $400K+ enterprise. Success hinges on keeping…

Read full answer ↗

Direct Answer Snowflake's 2024 credential-compromise incidents, affecting roughly 165 customers including Ticketmaster, Santander, and AT&T, permanently reshaped enterprise trust in cloud data platforms by exposing shared-responsibility mod…

Read full answer ↗

Direct Answer Snowflake's developer-platform strategy through 2027 centers on four pillars—Snowpark, Container Services, Streamlit-in-Snowflake, and the Native App Framework—designed to lock developers into warehouse-native compute and appl…

Read full answer ↗

Direct Answer By 2027, Snowflake should pursue a hybrid partnership strategy with Salesforce Data Cloud—locking contractual enterprise co-sell depth and Hyperforce neutrality while simultaneously building non-Salesforce data platform partne…

Read full answer ↗

How should Snowflake price Cortex agents — per query or per outcome? Direct Answer Snowflake should consider shifting from per-query to a hybrid per-outcome model, anchored to customer ROI (churn reduction, revenue lift, cycle time compress…

Read full answer ↗

Direct Answer Yes, Snowflake should eliminate credit-based pricing specifically for AI and Cortex workloads, transitioning to outcome-based models like per-token or per-message charges, while retaining credits for traditional compute such a…

Read full answer ↗

Direct Answer Streamlit needs a 2-3 year existential call by Q3 2026. Snowflake should NOT bet-the-farm on acquiring Gradio or chasing parity with Hugging Face Spaces (defensive spiral). Instead: stabilize Streamlit-in-Snowflake as a premiu…

Read full answer ↗

Direct Answer Snowflake should kill Cortex Apps as-is, consolidate Marketplace into 5-7 vertical industry bundles, and transform Snowsight into a standalone UI-intelligence layer that competes with AI-native data tools while licensing Corte…

Read full answer ↗

Direct Answer Buy Snowflake for predictable SQL-first analytics with mature public-company execution, or buy Databricks for AI/ML-native workloads with higher growth and open-source flexibility — your choice hinges on whether your primary d…

Read full answer ↗

Direct Answer Sridhar Ramaswamy's job is on the line in 2027 because Snowflake's board has set three concrete performance triggers: consecutive quarterly revenue misses, net revenue retention dropping below 105%, and Cortex AI attach rate f…

Read full answer ↗

Direct Answer By 2027, Snowflake generates over $5 billion in revenue by evolving beyond its core compute-storage model, with compute credits still dominant at ~72% of mix but increasingly supplemented by standalone Cortex AI tokens, Snowpa…

Read full answer ↗

Direct Answer Cortex AI is operationally live and shipping within Snowflake, but it remains undermonetized with an estimated attach rate of 8-15%, trailing Databricks Mosaic AI's 18-22% at a similar maturity stage. It functions as a competi…

Read full answer ↗

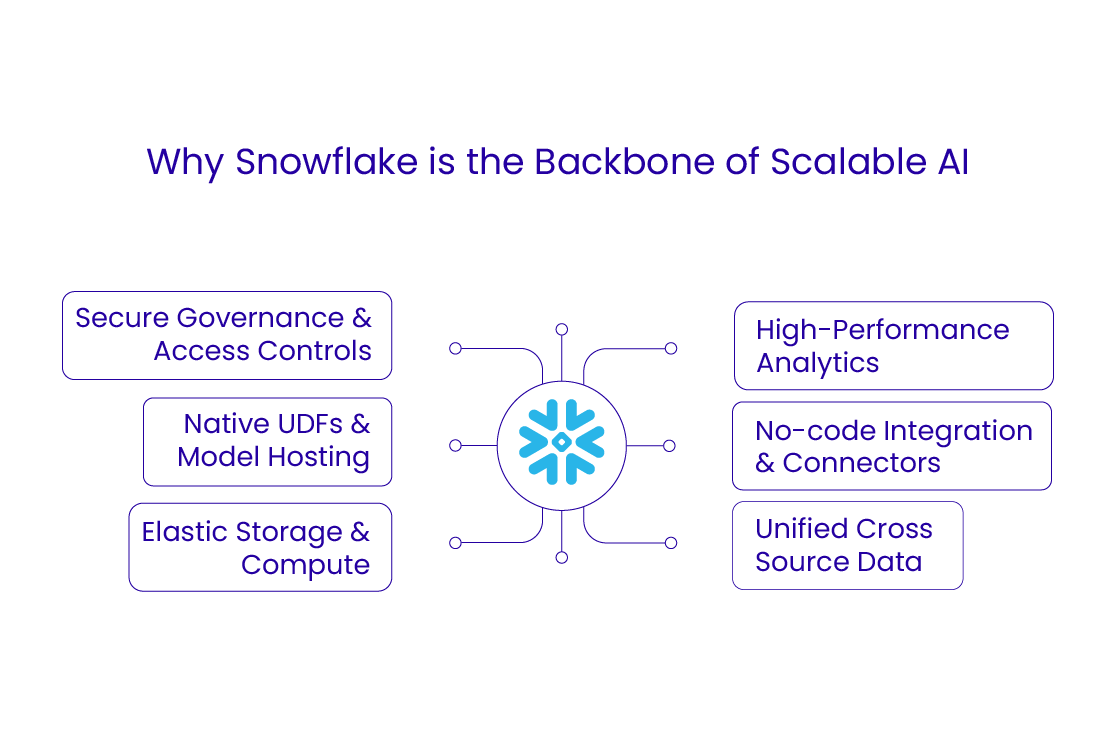

Direct Answer: Four Pillars Snowflake Must Own ![What is Snowflake AI strategy in 2027?](https://pulserevops.com/img/auto/q1564.…

Read full answer ↗

Direct Answer Yes, Snowflake can compete with Databricks in 2027, but only by doubling down on governance, data sharing, and compliance rather than trying to beat Databricks on AI/ML training velocity. Snowflake’s $3.5B revenue base and ent…

Read full answer ↗

Related topics in the library